European Indices Decline: DAX Down 0.96% Amid Broader Market Weakness — Cautious Sentiment.

· Market News · MarketsFN Team

🌍 European Indices Decline: DAX Down 0.96% Amid Broader Market Weakness — Cautious Sentiment.

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

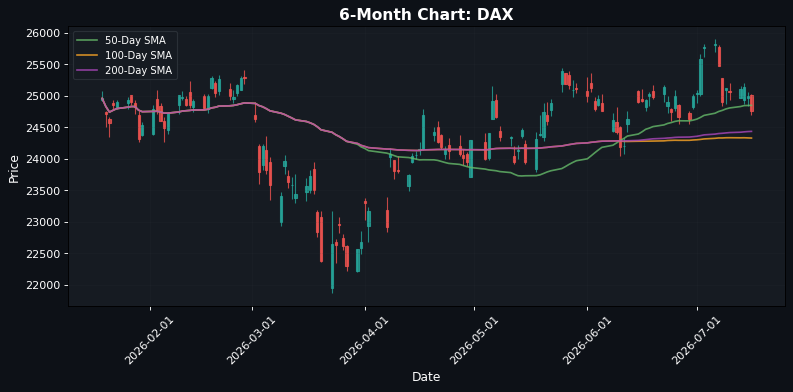

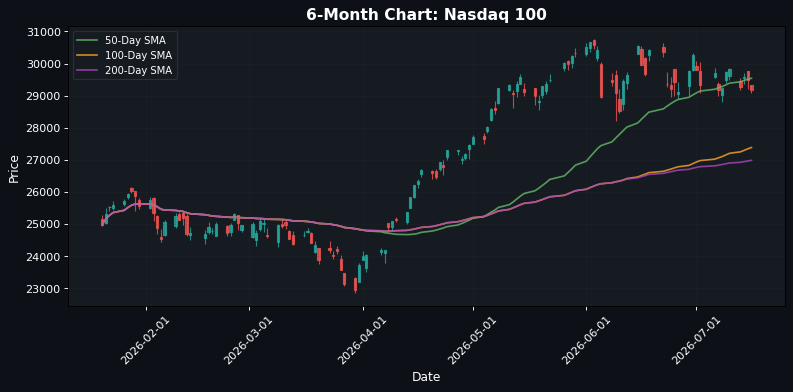

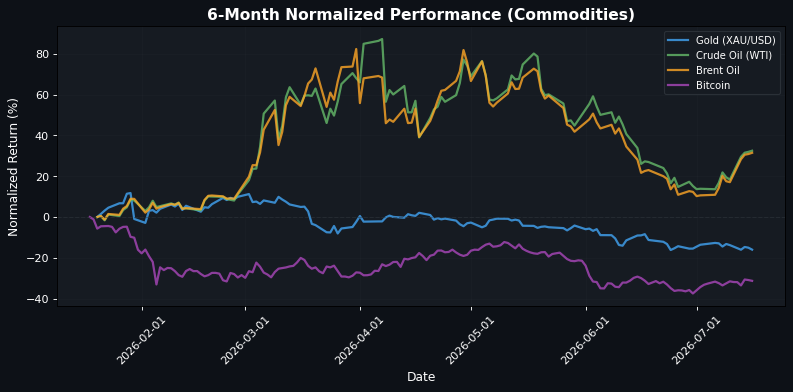

**Market Sentiment Dips Amid Global Economic Concerns** As European markets approach the close, a pervasive sense of caution is evident, with key indices reflecting a downward trend. The EuroStoxx 50 is down by 0.50% at 6234.38, while the DAX has fallen 0.96% to 24760.67. The FTSE 100 and CAC 40 also show declines of 0.39% and 0.81%, respectively. This bearish sentiment is echoed in the US markets, where the S&P 500 is down 0.31% at 7548.71 and the Nasdaq 100 has dropped 1.11% to 29176.39, indicating a broader risk-off attitude among investors. The backdrop for this market movement includes mixed signals from economic data. Notably, US Initial Jobless Claims decreased to 208K last week, suggesting a resilient labor market, yet the recent rise in US Retail Sales by only 0.2% to $768.6 billion raises concerns about consumer spending momentum. Additionally, the British Pound is under pressure, easing against the Yen after reaching its highest level since 2007, reflecting uncertainty around fiscal policies. In the commodities space, gold has tumbled by 1.13% to $3998.30, driven by ongoing inflation fears, while crude oil prices have shown slight gains, with WTI up 0.41% at $79.93. The EUR/USD pair is down 0.14% at 1.1453, highlighting the impact of policy divergence as the European Central Bank maintains a hawkish stance. Looking ahead, the market will be closely watching the upcoming US inflation data, which could significantly influence monetary policy expectations and either validate or challenge the current market sentiment.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6234.38 | -0.50% |

| DAX | 24760.67 | -0.96% |

| FTSE 100 | 10475.02 | -0.39% |

| CAC 40 | 8314.60 | -0.81% |

| FTSE MIB | 52027.78 | -0.73% |

| IBEX 35 | 19166.70 | -0.56% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7548.71 | -0.31% |

| Dow Jones | 52634.21 | -0.05% |

| Nasdaq 100 | 29176.39 | -1.11% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 66835.54 | -2.79% |

| Shanghai Composite | 3882.41 | -1.85% |

| Hang Seng | 25008.60 | +1.33% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.15 | -0.14% |

| GBP/USD | 1.35 | -0.19% |

| USD/JPY | 162.32 | +0.14% |

| Gold (XAU/USD) | 3998.30 | -1.13% |

| Crude Oil (WTI) | 79.93 | +0.41% |

| Brent Oil | 85.34 | +0.46% |

| Bitcoin | 64352.90 | -0.56% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by central bank signals and economic data releases. The European Central Bank maintains a hawkish stance, indicating a commitment to controlling inflation, which contrasts with the Bank of Canada's recent hold on interest rates, leading to a shift in guidance and pricing out future hikes. This divergence is impacting currency flows, particularly as the Euro experiences volatility against the US Dollar. In the US, initial jobless claims fell to 208K, suggesting a resilient labor market, while retail sales rose 0.2% in June to $768.6 billion, indicating steady consumer spending. However, inflation concerns persist, with energy-driven fears causing gold and silver prices to slip, as markets brace for potential Federal Reserve rate hikes. The British Pound is under pressure, easing against the Yen after reaching its highest level since 2007, amid fiscal uncertainties. Additionally, competition in the LNG market is creating storage challenges for natural gas, further complicating the energy landscape. These factors collectively signal a cautious outlook for markets, influenced by central bank policies and economic resilience.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 02:00 | GDP (MoM) (May) | High |

| 02:00 | Industrial Production (MoM) (May) | Medium |

| 02:00 | Manufacturing Production (MoM) (May) | Medium |

| 02:00 | Monthly GDP 3M/3M Change (May) | Medium |

| 02:00 | Trade Balance (May) | Medium |

| 02:00 | Trade Balance Non-EU (May) | Medium |

| 03:30 | SNB Monetary Policy Assessment | Medium |

| 05:00 | Trade Balance (May) | Medium |

| 08:00 | NIESR Monthly GDP Tracker (Jun) | Medium |

| 08:00 | Retail Sales (YoY) (May) | Medium |

| 08:00 | Retail Sales (MoM) (May) | Medium |

| 08:15 | Housing Starts (Jun) | Medium |

| 08:30 | Continuing Jobless Claims | Medium |

| 08:30 | Core Retail Sales (MoM) (Jun) | High |

| 08:30 | Initial Jobless Claims | High |

| 08:30 | Philadelphia Fed Manufacturing Index (Jul) | High |

| 08:30 | Philly Fed Employment (Jul) | Medium |

| 08:30 | Retail Control (MoM) (Jun) | Medium |

| 08:30 | Retail Sales (MoM) (Jun) | High |

| 10:00 | Business Inventories (MoM) (May) | Medium |

| 10:00 | Pending Home Sales (MoM) (Jun) | Medium |

| 10:00 | Retail Inventories Ex Auto (May) | Medium |

| 11:30 | Atlanta Fed GDPNow (Q2) | Medium |

| 16:30 | Fed's Balance Sheet | Medium |

| 21:00 | U.S. President Trump Speaks | High |

A series of key economic indicators will be released, including GDP, industrial production, and retail sales data, which are likely to provide insights into the overall economic health and consumer spending trends. The SNB's monetary policy assessment and the Fed's balance sheet update could influence market sentiment, particularly in currency and equity markets. Additionally, President Trump's speech may introduce political factors that could further impact market dynamics, depending on the content and implications of his remarks.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.