European Indices Decline: DAX Down 1.97% Amid Market Turmoil — Bearish Sentiment Prevails

· Market News · MarketsFN Team

🌍 European Indices Decline: DAX Down 1.97% Amid Market Turmoil — Bearish Sentiment Prevails

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

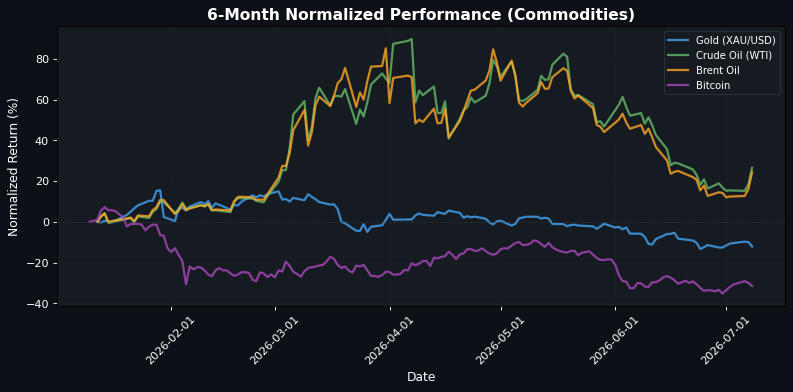

**Market Recap: European Indices Face Pressure Amid Geopolitical Tensions and Fed Speculation** European markets are closing sharply lower, reflecting a broader risk-off sentiment driven by geopolitical tensions and anticipation of hawkish signals from the upcoming Fed Minutes. The EuroStoxx 50 is down 1.60% at 6218.55, with the DAX and CAC 40 trailing closely at -1.97% and -1.99%, respectively. The IBEX 35 is the hardest hit, plunging 2.57% to 19136.40, as concerns over political stability in the UK add to the market's unease. In the US, indices are also in the red, with the S&P 500 down 0.77% at 7445.95 and the Dow Jones falling 1.41% to 52179.32. The Nasdaq 100 is faring slightly better, down just 0.59% at 28999.82, indicating a potential rotation towards tech amid the broader sell-off. The FX market reflects these tensions, with the Euro steadying above 1.1400 against the US Dollar at 1.1410, up 0.02%. Meanwhile, the British Pound is attempting a recovery, eyeing 1.36 against the Dollar, supported by high real yields in the UK. Commodities are experiencing mixed movements; gold is down 2.41% at 4045.3999, pressured by renewed US-Iran tensions that are reviving Fed rate hike bets, while crude oil prices are surging, with WTI up 6.91% at 75.3100. Looking ahead, all eyes will be on the Fed Minutes, which are expected to provide insights into the central bank's stance amid rising geopolitical risks. A hawkish tone could further strengthen the US Dollar and exacerbate the current market volatility.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6218.55 | -1.60% |

| DAX | 24963.11 | -1.97% |

| FTSE 100 | 10527.60 | -1.30% |

| CAC 40 | 8268.18 | -1.99% |

| FTSE MIB | 51885.84 | -1.09% |

| IBEX 35 | 19136.40 | -2.57% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7445.95 | -0.77% |

| Dow Jones | 52179.32 | -1.41% |

| Nasdaq 100 | 28999.82 | -0.59% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 68256.96 | -2.12% |

| Shanghai Composite | 3970.88 | -0.49% |

| Hang Seng | 24199.46 | +2.99% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.14 | +0.02% |

| GBP/USD | 1.34 | +0.14% |

| USD/JPY | 162.62 | +0.29% |

| Gold (XAU/USD) | 4045.40 | -2.41% |

| Crude Oil (WTI) | 75.31 | +6.91% |

| Brent Oil | 79.43 | +7.11% |

| Bitcoin | 61834.40 | -2.31% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by geopolitical tensions and central bank signals. The British Pound is attempting a recovery towards 1.36 against the US Dollar, as traders respond to potential shifts in UK political stability, with early election scenarios being discussed. Meanwhile, the US Dollar is supported by hawkish Fed minutes, which may reinforce rate hike expectations amid rising inflation concerns, particularly as oil prices increase. Geopolitical risks are heightened with renewed threats from Donald Trump regarding Iran, which have contributed to a decline in gold and silver prices, as investors anticipate a stronger US Dollar. The Euro remains steady above 1.1400, reflecting a balance between geopolitical concerns and ECB repricing. In Asia, India's gradual firming CPI suggests the RBI may maintain a patient stance, while New Zealand's RBNZ has hiked rates but cautioned about future moves. Additionally, Canada reports a trade surplus at a four-year high, indicating robust economic performance, although the Canadian Dollar faces strong resistance from the USD. Overall, these factors create a complex landscape for investors navigating currency and commodity markets.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 02:00 | CPI (YoY) (Jun) | Medium |

| 02:00 | CPI (MoM) (Jun) | Medium |

| 05:30 | German 10-Year Bund Auction | Medium |

| 07:30 | German Buba President Nagel Speaks | Medium |

| 08:49 | Interest Rate Decision (Jul) | Medium |

| 10:30 | Crude Oil Inventories | High |

| 10:30 | Cushing Crude Oil Inventories | Medium |

| 11:30 | Atlanta Fed GDPNow (Q2) | Medium |

| 12:40 | ECB's Schnabel Speaks | Medium |

| 13:00 | 10-Year Note Auction | High |

| 14:00 | FOMC Meeting Minutes | High |

| 15:00 | Consumer Credit (May) | Medium |

| 18:30 | Business NZ PMI (Jun) | Medium |

| 21:30 | CPI (YoY) (Jun) | Medium |

| 21:30 | CPI (MoM) (Jun) | Medium |

| 21:30 | PPI (YoY) (Jun) | Medium |

The upcoming economic events, particularly the Consumer Price Index (CPI) releases and interest rate decisions, are likely to significantly influence market sentiment, with potential volatility in equity and bond markets. The German Bund auction and speeches from key central bank officials may provide insights into monetary policy direction, impacting investor expectations. Additionally, crude oil inventory reports could affect energy prices, while the FOMC meeting minutes may reveal the Federal Reserve's stance on inflation and economic growth, further shaping market dynamics.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.