European Markets Decline: EuroStoxx 50 Down 1.14% — Risk Aversion Prevails Ahead of US Open

· Market News · MarketsFN Team

🌍 European Markets Decline: EuroStoxx 50 Down 1.14% — Risk Aversion Prevails Ahead of US Open

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

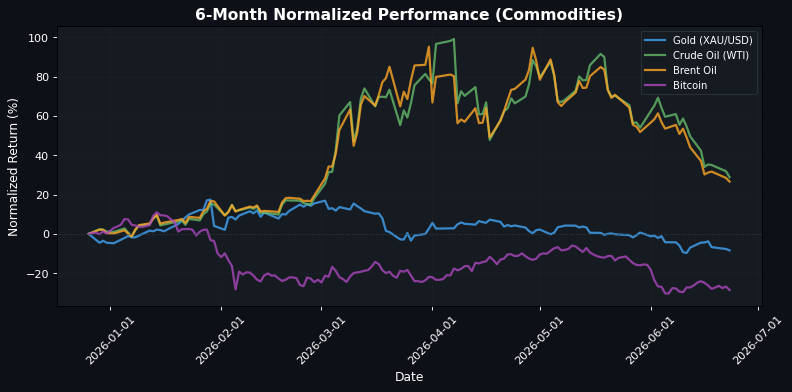

**Market Recap: Global Indices Retreat Amid Strengthening US Dollar and Commodity Pressures** Today’s market sentiment is heavily influenced by a strengthening US Dollar, which is climbing to one-year highs, leading to a broad-based sell-off across global indices. The EuroStoxx 50 is down 1.14% at 6239.50, with the DAX and CAC 40 also reflecting this bearish trend, declining 0.98% to 24893.89 and 0.59% to 8350.31, respectively. The FTSE MIB and IBEX 35 are not far behind, down 1.40% and 0.57%. In the US, the S&P 500 is down 0.97% at 7400.33, while the Nasdaq 100 is experiencing a more pronounced drop of 2.31% to 29645.97, indicating a tech sector under pressure. The Dow Jones is faring slightly better, down 0.32% at 51548.88. The FX markets are reacting to the dollar's strength, with EUR/USD at 1.1392, down 0.34%, and GBP/USD at 1.3213, down 0.31%. Commodities are also feeling the impact; gold is down 0.75% at 4150.3999, while crude oil prices are under pressure, with WTI down 2.27% at 73.1200 and Brent down 1.46% at 76.7600. The market is currently grappling with the implications of the US ADP Employment Change, which has seen a 4-week average increase to 30.75K, suggesting resilience in the labor market. This could further bolster the Fed's hawkish stance, adding to the dollar's strength. Looking ahead, the upcoming US S&P Global PMI data will be critical in assessing whether the resilient business activity narrative holds, potentially influencing both market sentiment and the dollar's trajectory.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6239.50 | -1.14% |

| DAX | 24893.89 | -0.98% |

| FTSE 100 | 10422.79 | -0.14% |

| CAC 40 | 8350.31 | -0.59% |

| FTSE MIB | 52058.74 | -1.40% |

| IBEX 35 | 19431.10 | -0.57% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7400.33 | -0.97% |

| Dow Jones | 51548.88 | -0.32% |

| Nasdaq 100 | 29645.97 | -2.31% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 69788.38 | -3.55% |

| Shanghai Composite | 4106.25 | -1.37% |

| Hang Seng | 23336.28 | -1.82% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.14 | -0.34% |

| GBP/USD | 1.32 | -0.31% |

| USD/JPY | 161.52 | -0.01% |

| Gold (XAU/USD) | 4150.40 | -0.75% |

| Crude Oil (WTI) | 73.12 | -2.27% |

| Brent Oil | 76.76 | -1.46% |

| Bitcoin | 62412.14 | -2.41% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by a mix of geopolitical tensions and central bank signals. The US Dollar is climbing to one-year highs, creating pressure on commodities like gold, which is now focusing on the $4,000 level. This strength in the dollar is compounded by the Federal Reserve's hawkish stance, which is keeping markets on edge regarding future interest rate movements. In the Eurozone, mixed PMI data indicates a two-speed recovery, challenging the European Central Bank's tightening narrative. The softer PMIs could hinder the ECB's ability to raise rates further, impacting the euro, which is testing 11-month lows against the dollar at 1.3991. On the employment front, the US ADP Employment Change 4-week average has risen to 30.75K, suggesting resilience in the labor market. Meanwhile, geopolitical risks are highlighted by the reopening of the Hormuz Strait, which is expected to soften oil prices for Brent and WTI. Additionally, the Japanese Yen faces intervention risks as it hits a 40-year low against the dollar, reflecting broader market anxieties.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 01:00 | BoJ Core CPI (YoY) | Medium |

| 01:00 | Core CPI (YoY) (May) | Medium |

| 01:00 | CPI (YoY) (May) | Medium |

| 03:15 | HCOB France Manufacturing PMI (Jun) | Medium |

| 03:15 | HCOB France Services PMI (Jun) | Medium |

| 03:30 | HCOB Germany Manufacturing PMI (Jun) | Medium |

| 03:30 | HCOB Germany Services PMI (Jun) | Medium |

| 04:00 | HCOB Eurozone Manufacturing PMI (Jun) | Medium |

| 04:00 | HCOB Eurozone Composite PMI (Jun) | Medium |

| 04:00 | HCOB Eurozone Services PMI (Jun) | Medium |

| 04:30 | S&P Global Composite PMI (Jun) | Medium |

| 04:30 | S&P Global Manufacturing PMI (Jun) | Medium |

| 04:30 | S&P Global Services PMI (Jun) | Medium |

| 04:30 | ECB's Lane Speaks | Medium |

| 04:35 | German Buba Mauderer Speaks | Medium |

| 08:15 | ADP Employment Change Weekly | Medium |

| 09:00 | BoC Gov Macklem Speaks | Medium |

| 09:15 | ECB's Elderson Speaks | Medium |

| 09:45 | S&P Global Manufacturing PMI (Jun) | High |

| 09:45 | S&P Global Composite PMI (Jun) | Medium |

| 09:45 | S&P Global Services PMI (Jun) | High |

| 13:00 | 2-Year Note Auction | Medium |

| 16:30 | API Weekly Crude Oil Stock | Medium |

| 21:30 | Trimmed Mean CPI (QoQ) | Medium |

A series of key economic indicators are set to be released, including CPI data from Japan and various PMIs from France, Germany, and the Eurozone, which will provide insights into inflation and manufacturing activity. The outcomes of these reports, particularly the Core CPI and PMIs, could significantly influence market sentiment, potentially affecting central bank policies and investor confidence. Additionally, speeches from central bank officials may further shape market expectations regarding interest rates and economic outlook.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.