FTSE 100 Rises 0.22%: UK Stocks Show Resilience Amid Mixed European Markets — Positive Outlook

· Market News · MarketsFN Team

🌍 FTSE 100 Rises 0.22%: UK Stocks Show Resilience Amid Mixed European Markets — Positive Outlook

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

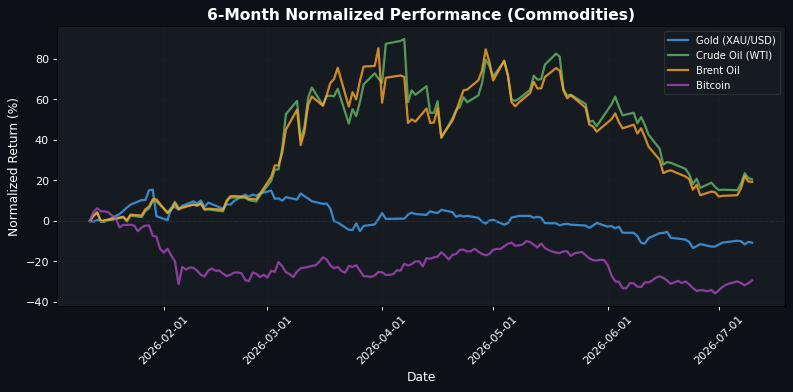

**Market Resilience Amid Mixed Signals: European Indices Struggle While US Markets Show Modest Gains** As European markets approach the close, a mixed sentiment prevails, with the EuroStoxx 50 down by -0.18% at 6272.84, reflecting a cautious outlook. The DAX and CAC 40 also dipped slightly, down -0.07% to 25100.03 and -0.03% to 8323.84, respectively. In contrast, the FTSE 100 managed a modest gain of +0.22% to 10495.36, buoyed by strength in the UK economy, while the FTSE MIB and IBEX 35 rose by +0.67% and +0.58%, respectively, indicating regional pockets of resilience. Across the Atlantic, US indices are showing slight upward momentum, with the S&P 500 up +0.17% at 7556.46 and the Dow Jones gaining +0.14% to 52558.43. However, the Nasdaq 100 is marginally down by -0.04% at 29714.54, reflecting ongoing concerns about tech valuations amidst the AI boom narrative. In the FX and commodities space, the EUR/USD is down -0.10% to 1.1423, while the GBP/USD is slightly up by +0.02% to 1.3406. Crude oil prices are under pressure, with WTI down -0.46% to 71.7500, as market participants weigh the implications of geopolitical tensions in the Strait of Hormuz against hopes for US-Iran de-escalation. The forward-looking catalyst to watch is the upcoming US inflation data, which could significantly influence market sentiment and Fed policy expectations. A surprise in either direction could lead to increased volatility across both equity and commodity markets, particularly in light of the recent adjustments to Core PCE inflation methodology.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6272.84 | -0.18% |

| DAX | 25100.03 | -0.07% |

| FTSE 100 | 10495.36 | +0.22% |

| CAC 40 | 8323.84 | -0.03% |

| FTSE MIB | 52730.80 | +0.67% |

| IBEX 35 | 19434.60 | +0.58% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7556.46 | +0.17% |

| Dow Jones | 52558.43 | +0.14% |

| Nasdaq 100 | 29714.54 | -0.04% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 68557.73 | +1.20% |

| Shanghai Composite | 3996.16 | -1.00% |

| Hang Seng | 24175.12 | +0.60% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.14 | -0.10% |

| GBP/USD | 1.34 | +0.02% |

| USD/JPY | 161.78 | -0.36% |

| Gold (XAU/USD) | 4110.30 | -0.49% |

| Crude Oil (WTI) | 71.75 | -0.46% |

| Brent Oil | 76.21 | -0.12% |

| Bitcoin | 64419.00 | +1.94% |

🌍 Geopolitics and Market Drivers

Recent market movements are significantly influenced by a mix of economic data and geopolitical developments. In Canada, the unemployment rate declined to 6.5% in June, bolstering the Canadian Dollar as the jobs report exceeded forecasts. However, TD Securities warns of potential softening in labor data, indicating mixed signals for the currency. Meanwhile, Mexico's softer CPI supports a dovish stance from Banxico, which could impact the Peso's performance. Geopolitically, Qatar's mediation efforts with Iran aim to ease tensions over the Strait of Hormuz, contributing to stability in oil prices, with WTI holding near $72 amid hopes for US-Iran de-escalation. This backdrop is critical as it affects global energy markets and inflation expectations. Additionally, the Eurozone's economic data suggests a potential pause from the ECB, influencing the Euro's retracement. The Australian Dollar's rise, driven by a hawkish RBA and diplomatic pressures on the USD, reflects shifting central bank dynamics. Overall, these factors create a complex landscape for currencies and commodities, with central bank signals and geopolitical tensions at the forefront.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 02:00 | German CPI (MoM) (Jun) | High |

| 02:00 | German CPI (YoY) (Jun) | Medium |

| 02:45 | French CPI (MoM) (Jun) | Medium |

| 02:45 | French HICP (MoM) (Jun) | Medium |

| 03:00 | SECO Consumer Climate (Jun) | Medium |

| 05:00 | IEA Monthly Report | Medium |

| 08:00 | CPI (YoY) (Jun) | Medium |

| 08:30 | Building Permits (MoM) (May) | Medium |

| 08:30 | Employment Change (Jun) | Medium |

| 08:30 | Unemployment Rate (Jun) | Medium |

| 12:00 | WASDE Report | Medium |

| 12:00 | CPI (MoM) (Jun) | Medium |

| 12:00 | CPI (YoY) (Jun) | Medium |

| 13:00 | U.S. Baker Hughes Oil Rig Count | Medium |

| 13:00 | U.S. Baker Hughes Total Rig Count | Medium |

| 15:30 | CFTC GBP speculative net positions | Medium |

| 15:30 | CFTC Crude Oil speculative net positions | Medium |

| 15:30 | CFTC Gold speculative net positions | Medium |

| 15:30 | CFTC Nasdaq 100 speculative net positions | Medium |

| 15:30 | CFTC S&P 500 speculative net positions | Medium |

| 15:30 | CFTC AUD speculative net positions | Medium |

| 15:30 | CFTC BRL speculative net positions | Medium |

| 15:30 | CFTC JPY speculative net positions | Medium |

| 15:30 | CFTC EUR speculative net positions | Medium |

The release of various Consumer Price Index (CPI) data from Germany and France, along with the U.S. CPI and employment figures, is likely to influence market sentiment regarding inflation and economic growth. Higher-than-expected inflation readings may lead to increased volatility in equity markets and pressure on central banks to adjust monetary policy. Additionally, the IEA Monthly Report and the Baker Hughes rig counts could impact oil prices, while the CFTC speculative positions data may provide insights into market sentiment across various asset classes.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.