S&P 500 Up 0.77%: Strong Gains Lead US Markets — Positive Momentum Continues

· Market News · MarketsFN Team

🌍 S&P 500 Up 0.77%: Strong Gains Lead US Markets — Positive Momentum Continues

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

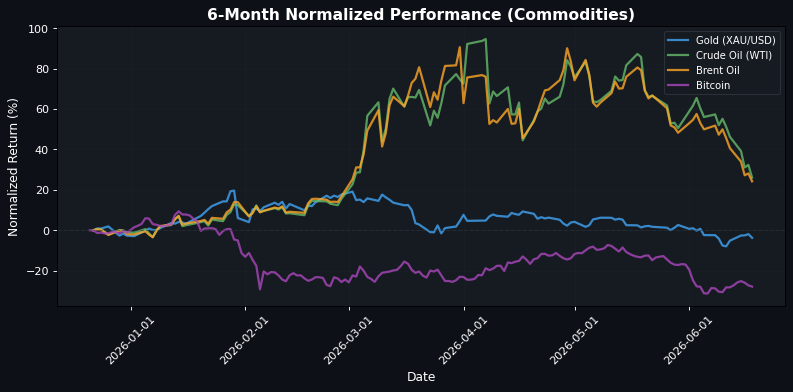

**US Markets Rally as European Indices Struggle with Mixed Sentiment** As US markets remain active, the S&P 500 has gained +0.77% to 7477.32, driven by a robust performance in the tech sector, particularly the Nasdaq 100, which surged +1.65% to 30160.23. This upward momentum contrasts sharply with the European indices, where the EuroStoxx 50 is up only +0.19% at 6311.90, while the FTSE 100 has declined -1.06% to 10397.14, reflecting a more cautious sentiment across the Atlantic. The divergence in performance highlights a critical cross-market dynamic: while US investors are buoyed by positive economic indicators, including a drop in initial jobless claims to 226K, European markets are grappling with mixed signals from the ECB. ECB’s Lane has indicated that further rate hikes are justified, even amid a milder economic outlook, which has contributed to a lack of conviction among European investors. The FTSE 100's decline is particularly notable as the British Pound hits fresh two-month lows below 1.3220 against the Euro, following the BoE's decision to maintain rates. In the commodities space, crude oil prices have taken a hit, with WTI down -4.75% to 73.1400, exacerbated by a hawkish Fed outlook and weaker oil demand, which has pressured currencies like the Canadian Dollar. Gold has also fallen -1.85% to 4278.1001, reflecting a risk-off sentiment. Looking ahead, the upcoming US inflation data will be pivotal. A stronger-than-expected reading could further bolster US equities and reinforce the Fed's hawkish stance, while a softer print may shift market dynamics, potentially narrowing the gap between US and European performance.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6311.90 | +0.19% |

| DAX | 24959.93 | +0.10% |

| FTSE 100 | 10397.14 | -1.06% |

| CAC 40 | 8445.18 | +0.17% |

| FTSE MIB | 52539.39 | -0.11% |

| IBEX 35 | 19363.70 | -0.30% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7477.32 | +0.77% |

| Dow Jones | 51722.35 | +0.45% |

| Nasdaq 100 | 30160.23 | +1.65% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 71053.49 | +1.65% |

| Shanghai Composite | 4090.48 | -0.43% |

| Hang Seng | 23924.81 | -1.59% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.15 | -0.29% |

| GBP/USD | 1.32 | -0.44% |

| USD/JPY | 160.91 | +0.23% |

| Gold (XAU/USD) | 4278.10 | -1.85% |

| Crude Oil (WTI) | 73.14 | -4.75% |

| Brent Oil | 77.11 | -3.07% |

| Bitcoin | 63889.87 | -0.82% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by central bank signals and economic data releases. The U.S. Initial Jobless Claims dropped to 226K last week, indicating a resilient labor market, which aligns with the Federal Reserve's hawkish outlook, subsequently pressuring the Canadian Dollar as oil prices weaken. The European Central Bank's (ECB) Chief Economist, Philip Lane, emphasized that further rate hikes remain justified, even amid a milder economic outlook, suggesting a commitment to tightening monetary policy. In the UK, the Bank of England (BoE) maintained its bank rate at 3.75%, leading to the British Pound hitting fresh two-month lows below 1.3220 against the Euro, which is rallying as it reflects a stronger position amid the BoE's steady policy path. Meanwhile, the Norwegian Krone is supported by a hawkish hold from Norges Bank, raising prospects for an August rate hike. Overall, these central bank decisions and economic indicators are creating a complex landscape, with currencies reacting sharply to divergent monetary policies and economic signals.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 02:00 | Average Earnings Index +Bonus (Apr) | Medium |

| 02:00 | Claimant Count Change (May) | Medium |

| 02:00 | Employment Change 3M/3M (MoM) (Apr) | Medium |

| 02:00 | Unemployment Rate (Apr) | Medium |

| 03:00 | German Buba President Nagel Speaks | Medium |

| 03:30 | SNB Interest Rate Decision (Q2) | High |

| 03:30 | SNB Monetary Policy Assessment | Medium |

| 03:30 | Interest Rate Decision | Medium |

| 04:00 | Interest Rate (Q2) | Medium |

| 04:00 | Interest Rate Decision | Medium |

| 04:30 | SNB Press Conference | Medium |

| 06:10 | ECB's Elderson Speaks | Medium |

| 07:00 | BoE MPC vote cut (Jun) | Medium |

| 07:00 | BoE MPC vote hike (Jun) | Medium |

| 07:00 | BoE MPC vote unchanged (Jun) | Medium |

| 07:00 | BoE Interest Rate Decision (Jun) | High |

| 07:00 | BoE MPC Meeting Minutes | Medium |

| 08:15 | ECB's Lane Speaks | Medium |

| 08:30 | Continuing Jobless Claims | Medium |

| 08:30 | Initial Jobless Claims | High |

| 08:30 | Philadelphia Fed Manufacturing Index (Jun) | High |

| 08:30 | Philly Fed Employment (Jun) | Medium |

| 08:30 | RMPI (MoM) (May) | Medium |

| 10:00 | US Leading Index (MoM) (May) | Medium |

| 13:00 | U.S. Baker Hughes Oil Rig Count | Medium |

| 13:00 | U.S. Baker Hughes Total Rig Count | Medium |

| 16:00 | TIC Net Long-Term Transactions (Apr) | Medium |

| 16:30 | Fed's Balance Sheet | Medium |

| 19:30 | National Core CPI (YoY) (May) | Medium |

| 19:50 | Monetary Policy Meeting Minutes | Medium |

| 19:50 | National CPI (MoM) (May) | Medium |

A series of significant economic indicators are set to be released, including the Average Earnings Index, Claimant Count Change, and Unemployment Rate, which could influence market sentiment regarding labor market strength and wage growth. Additionally, central bank decisions from the Swiss National Bank (SNB) and the Bank of England (BoE) regarding interest rates will be closely watched, as any changes or hints of future policy shifts could lead to volatility in currency and equity markets. The release of U.S. jobless claims and manufacturing indices will also provide insights into the economic outlook, potentially impacting investor confidence and market direction.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.