BDCs Simplified: The Complete Guide to High-Yield Private Credit Investing

· Alternative Investments · MarketsFN Editorial

BDCs Simplified: The Complete Guide to High-Yield Private Credit Investing

Published: June 05, 2026 · MarketsFN Editorial

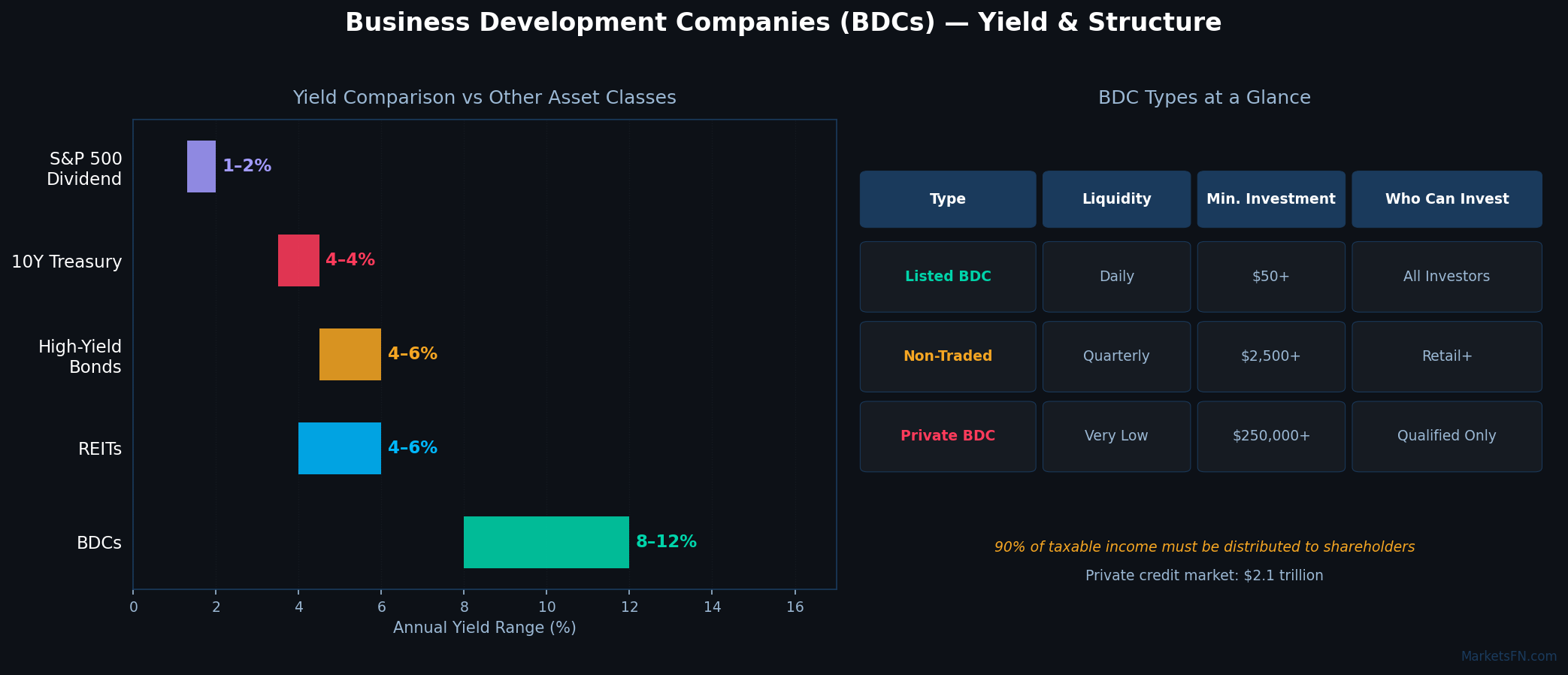

For many individual investors, the world of private equity and private credit has long been behind a velvet rope, accessible only to institutional giants and the ultra-wealthy. Business Development Companies (BDCs) have changed this dynamic, offering everyday investors a transparent, liquid window into the $2.1 trillion private credit market.

What Exactly is a BDC?

A Business Development Company is a unique investment vehicle established by the U.S. Congress in 1980. Its primary mission is to fuel the growth of small and mid-sized U.S. businesses. Think of a BDC as a hybrid between a traditional bank and a private equity firm: like a bank, they lend money and collect interest; like a private equity firm, they often take ownership stakes in the companies they support.

The companies BDCs invest in are typically in early stages of development or are "distressed" entities that cannot secure loans from traditional banks. By stepping into this gap, BDCs provide essential funding to the middle market of the American economy.

The Income Engine: How BDCs Generate High Yield

BDCs typically pay dividends of 8% to 12% per year — not by accident, but by law. To qualify as a Regulated Investment Company (RIC) and avoid corporate-level income taxes, a BDC must distribute at least 90% of its taxable income to shareholders every year. This is very similar to how REITs work.

While a tech giant like Google reinvests profits into R&D, a BDC must hand those profits directly to investors. This makes BDCs a "pure play" on the interest income and capital gains generated by their portfolio of private companies.

Management Styles: Internal vs. External

The Risks: Why BDCs Are Not Risk-Free

- Credit Risk: BDCs lend to riskier companies than those in the S&P 500. Defaults hurt NAV.

- Interest Rate Risk: Rising rates increase borrowing costs, squeezing margins even for floating-rate lenders.

- Share Dilution: Since 90% of earnings must be paid out, BDCs issue new shares frequently to grow — which can dilute existing holders.

How to Analyse a BDC: 3 Key Metrics

| Metric | What It Measures | What to Look For |

|---|---|---|

| Net Asset Value (NAV) | "Book value" of assets minus liabilities | Growing NAV over time |

| Price-to-NAV Ratio | Market price vs. book value | Avoid paying large premiums; discounts can be value |

| Dividend Sustainability | Is NII covering the dividend? | NII per share should exceed dividend per share |

The Tax Reality

BDC dividends are typically taxed at your ordinary income rate, not the lower 15% qualified dividend rate. However, because the raw payout is so much higher (8–12% vs. 2–3% for blue chips), most income-focused investors still come out ahead after tax. BDCs issue a standard 1099 — not a K-1 — making tax filing straightforward.

Beginner Portfolio Strategy

Financial experts recommend limiting BDC exposure to 10–25% of a total portfolio. A healthy mix of BDCs, stable blue-chip stocks, and REITs provides a balanced income stream. If you prefer not to pick individual stocks, the VanEck BDC Income ETF (BIZD) offers a diversified basket of the largest BDCs in a single ticker.

The golden rule: don't chase the highest yield — chase the highest quality. A 20% dividend that erodes NAV steadily is far worse than a 9% dividend backed by consistent Net Investment Income growth.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice or investment recommendations. All investments involve risks and past performance does not guarantee future results.