European Indices Decline: EuroStoxx 50 Down 0.85% — Market Sentiment Weakens.

· Market News · MarketsFN Team

🌍 European Indices Decline: EuroStoxx 50 Down 0.85% — Market Sentiment Weakens.

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

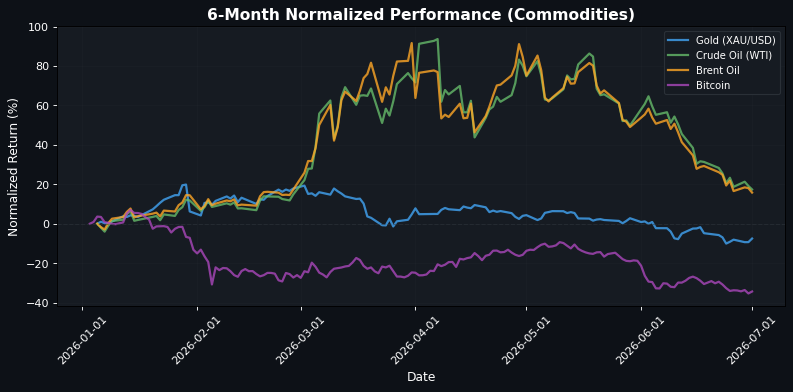

**Market Sentiment Dips Amid Mixed Economic Signals and Commodity Pressure** European markets are closing lower, reflecting a cautious sentiment as investors digest mixed economic indicators and ongoing commodity price pressures. The EuroStoxx 50 is down by 0.85% at 6274.11, with the CAC 40 leading the decline at -0.98% to 8321.30. The DAX and FTSE 100 are also in the red, down 0.08% and 0.50%, respectively. This downward trend is compounded by the recent drop in the US ISM Manufacturing PMI to 53.3 in June, signaling potential slowing in economic activity. In the US, the S&P 500 is slightly down by 0.02% at 7498.07, while the Dow Jones shows a modest gain of 0.26% at 52454.04, indicating a divergence in investor sentiment across sectors. The Nasdaq 100, however, is feeling the pressure, down 1.13% at 29933.07, reflecting concerns over tech valuations amid rising interest rates. In the FX markets, the EUR/USD pair is down 0.25% at 1.1399, influenced by Fed Chair Warsh's remarks emphasizing dissatisfaction with inflation levels above 2%, which has also supported the Swiss Franc as the US Dollar eases. Commodities are under pressure, with gold rising 2.00% to $4103.50, likely as a safe haven amid market volatility, while crude oil prices are down sharply, with WTI at $68.45 (-1.51%) and Brent at $71.52 (-1.92%). Looking ahead, the market will closely watch upcoming inflation data and central bank communications, particularly any shifts in the Federal Reserve's stance on interest rates, which could significantly impact market dynamics and investor sentiment.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6274.11 | -0.85% |

| DAX | 24975.68 | -0.08% |

| FTSE 100 | 10444.82 | -0.50% |

| CAC 40 | 8321.30 | -0.98% |

| FTSE MIB | 51488.59 | -0.37% |

| IBEX 35 | 19372.70 | -0.51% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7498.07 | -0.02% |

| Dow Jones | 52454.04 | +0.26% |

| Nasdaq 100 | 29933.07 | -1.13% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 70062.32 | +0.86% |

| Shanghai Composite | 4112.45 | +0.44% |

| Hang Seng | 22881.02 | -0.63% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.14 | -0.25% |

| GBP/USD | 1.33 | +0.12% |

| USD/JPY | 162.39 | -0.09% |

| Gold (XAU/USD) | 4103.50 | +2.00% |

| Crude Oil (WTI) | 68.45 | -1.51% |

| Brent Oil | 71.52 | -1.92% |

| Bitcoin | 59459.40 | +1.54% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by central bank signals and economic data releases. The US ISM Manufacturing PMI dropped to 53.3 in June, indicating potential weakness in the manufacturing sector, which may prompt the Federal Reserve to reassess its monetary policy stance. Fed Chair Warsh's remarks highlight concerns over inflation remaining above the 2% target, suggesting a cautious approach moving forward. In Europe, the European Central Bank has noted reduced risks for July due to softer economic data, while Lagarde's speech indicates a more balanced risk outlook compared to previous weeks. The Bank of England's Bailey has ruled out rate cuts for now, keeping the British Pound's rates curve elevated amid ongoing inflation risks. Geopolitically, the Japanese Yen remains under pressure, hitting 40-year lows, as authorities appear to be passive despite a surge in the Tankan index. The New Zealand Dollar is declining due to safe-haven demand for the US Dollar, particularly ahead of the Non-Farm Payrolls report. Overall, these factors suggest a cautious market sentiment with potential volatility ahead.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 02:00 | Nationwide HPI (MoM) (Jun) | Medium |

| 02:00 | Nationwide HPI (YoY) (Jun) | Medium |

| 03:15 | HCOB Spain Manufacturing PMI (Jun) | Medium |

| 03:30 | procure.ch Manufacturing PMI (Jun) | Medium |

| 03:45 | HCOB Italy Manufacturing PMI (Jun) | Medium |

| 03:50 | HCOB France Manufacturing PMI (Jun) | Medium |

| 03:55 | HCOB Germany Manufacturing PMI (Jun) | Medium |

| 04:00 | HCOB Eurozone Manufacturing PMI (Jun) | Medium |

| 04:30 | S&P Global Manufacturing PMI (Jun) | Medium |

| 05:00 | Core CPI (YoY) (Jun) | Medium |

| 05:00 | CPI (YoY) (Jun) | High |

| 05:00 | CPI (MoM) (Jun) | Medium |

| 06:15 | ECB's Lane Speaks | Medium |

| 07:45 | FOMC Member Daly Speaks | Medium |

| 08:15 | ADP Nonfarm Employment Change (Jun) | High |

| 09:00 | BoE Gov Bailey Speaks | Medium |

| 09:00 | Fed Governor Warsh Speaks | Medium |

| 09:00 | BoC Gov Macklem Speaks | Medium |

| 09:00 | ECB President Lagarde Speaks | Medium |

| 09:45 | S&P Global Manufacturing PMI (Jun) | High |

| 10:00 | Construction Spending (MoM) (May) | Medium |

| 10:00 | ISM Manufacturing Employment (Jun) | Medium |

| 10:00 | ISM Manufacturing PMI (Jun) | High |

| 10:00 | ISM Manufacturing Prices (Jun) | High |

| 10:30 | Crude Oil Inventories | High |

| 10:30 | Cushing Crude Oil Inventories | Medium |

| 10:30 | ECB President Lagarde Speaks | Medium |

| 11:30 | Atlanta Fed GDPNow (Q2) | Medium |

| 12:00 | GDP Monthly (YoY) (May) | Medium |

| 12:00 | Retail Sales (YoY) (May) | Medium |

| 12:00 | Unemployment Rate (May) | Medium |

| 15:15 | U.S. President Trump Speaks | High |

| 21:30 | Trade Balance (May) | Medium |

| 23:35 | 10-Year JGB Auction | Medium |

A series of significant economic reports and speeches are scheduled, including key indicators like the CPI, Manufacturing PMI, and employment changes, which could influence market sentiment and volatility. The release of inflation data, particularly the Core CPI and overall CPI, is critical as it may impact central bank policies and investor expectations regarding interest rates. Additionally, speeches from various central bank officials, including the ECB and Fed, could provide insights into future monetary policy directions, further affecting market dynamics.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.