European Markets Decline: EuroStoxx 50 Down 0.82% — Bearish Sentiment Prevails.

· Market News · MarketsFN Team

🌍 European Markets Decline: EuroStoxx 50 Down 0.82% — Bearish Sentiment Prevails.

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

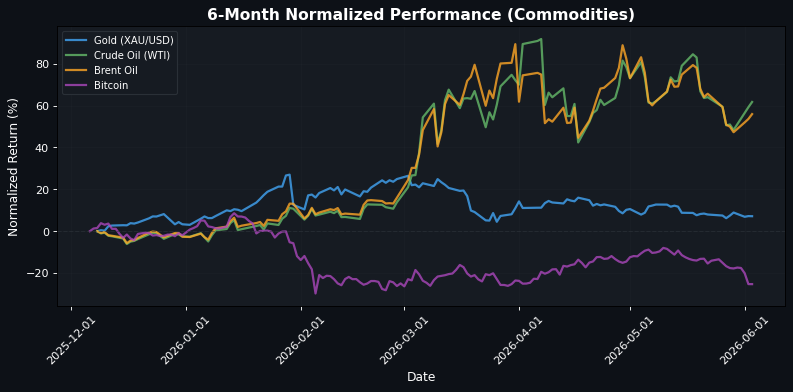

**Market Sentiment Dips as European Indices Slide Amidst Mixed Economic Signals** European markets are closing in the red, reflecting a broader risk-off sentiment as investors digest mixed economic data and central bank signals. The EuroStoxx 50 fell by 0.82% to 6058.05, with the DAX down 1.40% at 24771.63, indicating a significant retreat in investor confidence. The FTSE 100 and CAC 40 also experienced declines of 0.36% and 0.57%, respectively, as the market grapples with inflationary pressures and potential interest rate adjustments. In the US, the S&P 500 is down 0.38% at 7580.49, while the Dow Jones has dropped 0.76% to 50919.69. The Nasdaq 100 is slightly more resilient, down just 0.03% at 30652.75. This divergence suggests that tech stocks may be holding up better amid the broader market pullback, potentially due to their growth-oriented nature in a high-rate environment. Currency markets reflect this cautious sentiment, with the EUR/USD trading at 1.1612, down 0.21%, and the GBP/USD at 1.3433, down 0.25%. The US Dollar remains firm, bolstered by the recent ISM Services PMI data, which rose to 54.4, exceeding expectations and reinforcing the Fed's current policy stance as articulated by Fed's Williams, who noted no immediate need for rate changes. In commodities, crude oil prices are on the rise, with WTI up 1.58% at 95.2400, indicating potential supply concerns amidst geopolitical tensions. However, gold remains under pressure, down 0.05% at 4486.8999, as inflation fears are countered by risk aversion. Looking ahead, the market will be closely watching upcoming economic indicators, particularly the US Non-Farm Payrolls report, which could provide further clarity on labor market strength and influence Fed policy direction.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6058.05 | -0.82% |

| DAX | 24771.63 | -1.40% |

| FTSE 100 | 10336.29 | -0.36% |

| CAC 40 | 8161.98 | -0.57% |

| FTSE MIB | 50133.33 | -0.88% |

| IBEX 35 | 18223.90 | -0.26% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7580.49 | -0.38% |

| Dow Jones | 50919.69 | -0.76% |

| Nasdaq 100 | 30652.75 | -0.03% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 66734.24 | -0.30% |

| Shanghai Composite | 4083.97 | +0.22% |

| Hang Seng | 25633.21 | -1.56% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.16 | -0.21% |

| GBP/USD | 1.34 | -0.25% |

| USD/JPY | 159.96 | +0.05% |

| Gold (XAU/USD) | 4486.90 | -0.05% |

| Crude Oil (WTI) | 95.24 | +1.58% |

| Brent Oil | 97.46 | +1.52% |

| Bitcoin | 66680.25 | -0.04% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by several key geopolitical and macroeconomic factors. The Japanese Yen is experiencing limited downside against the US Dollar as the Bank of Japan signals a potential interest rate hike, indicating a shift in monetary policy that could strengthen the Yen. In the US, Fed's Williams stated that current policy is appropriately set, suggesting no imminent changes to interest rates, which supports a stable outlook for the Dollar amidst risk aversion. Economic data releases are pivotal; the US ISM Services PMI rose to 54.4 in May, exceeding expectations and reinforcing the Dollar's strength. Conversely, the S&P Global Services PMI missed estimates, highlighting mixed signals in the US economy. Geopolitically, tensions in the Gulf region have led to a surge in WTI Crude Oil prices, compounded by a sharp drawdown in US inventories. Additionally, the Swiss Franc has weakened against the Dollar following strong ADP and ISM Services PMI data, reflecting market reactions to economic performance. Overall, these factors create a complex landscape for investors, balancing growth signals against geopolitical risks.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 02:00 | S&P Global Services PMI (May) | Medium |

| 03:15 | HCOB Spain Services PMI (May) | Medium |

| 03:45 | HCOB Italy Services PMI (May) | Medium |

| 03:50 | HCOB France Services PMI (May) | Medium |

| 03:55 | HCOB Germany Services PMI (May) | Medium |

| 04:00 | HCOB Eurozone Composite PMI (May) | Medium |

| 04:00 | HCOB Eurozone Services PMI (May) | Medium |

| 04:30 | S&P Global Composite PMI (May) | Medium |

| 04:30 | S&P Global Services PMI (May) | Medium |

| 05:50 | ECB's Elderson Speaks | Medium |

| 08:00 | Industrial Production (YoY) (Apr) | Medium |

| 08:15 | ADP Nonfarm Employment Change (May) | High |

| 08:30 | Labor Productivity (QoQ) (Q1) | Medium |

| 09:00 | Fed Vice Chair for Supervision Barr Speaks | Medium |

| 09:45 | S&P Global Composite PMI (May) | Medium |

| 09:45 | S&P Global Services PMI (May) | High |

| 10:00 | Factory Orders (MoM) (Apr) | Medium |

| 10:00 | ISM Non-Manufacturing Employment (May) | Medium |

| 10:00 | ISM Non-Manufacturing PMI (May) | High |

| 10:00 | ISM Non-Manufacturing Prices (May) | High |

| 10:30 | Crude Oil Inventories | High |

| 10:30 | Cushing Crude Oil Inventories | Medium |

| 12:00 | Retail Sales (YoY) (Apr) | Medium |

| 12:00 | Unemployment Rate (Apr) | Medium |

| 12:29 | GDP Monthly (YoY) (Apr) | Medium |

| 14:00 | Beige Book | Medium |

| 21:30 | Trade Balance (Apr) | Medium |

A series of key economic indicators, including various PMIs across Europe and the U.S., will be released, providing insights into service sector performance and overall economic health. The ADP Nonfarm Employment Change and ISM Non-Manufacturing PMI are particularly significant, as they may influence market sentiment regarding employment trends and economic growth. Additionally, speeches from ECB and Fed officials could further impact market expectations around monetary policy, while retail sales and unemployment data will be critical for gauging consumer strength and labor market conditions.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.