European Markets Mixed: FTSE 100 Up 0.74% While DAX Falls 0.72% — Divergent Trends Persist.

· Market News · MarketsFN Team

🌍 European Markets Mixed: FTSE 100 Up 0.74% While DAX Falls 0.72% — Divergent Trends Persist.

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

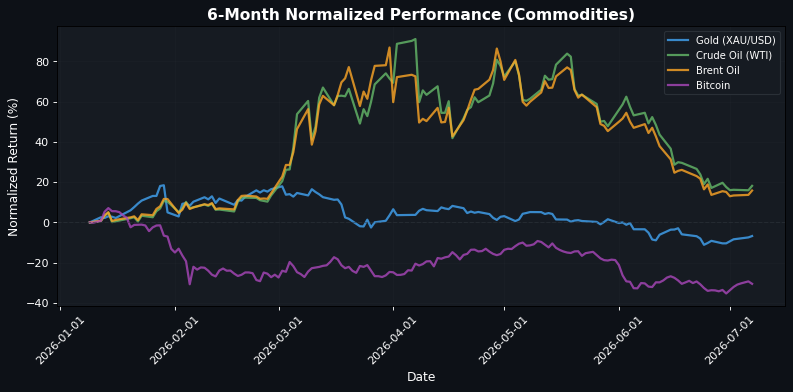

**Market Recap: Diverging Trends as European Indices Show Resilience Amidst US Weakness** As European markets approach the close, a notable divergence is evident between the indices, with the FTSE 100 leading the charge, up +0.74% at 10730.68, while the DAX and EuroStoxx 50 lag behind, down -0.72% at 25631.47 and -0.55% at 6362.83, respectively. This mixed performance underscores a broader theme of resilience in select markets, particularly in the UK and Spain, where the IBEX 35 is up +0.54% at 19789.60. The CAC 40 also shows slight gains, up +0.17% at 8494.28, indicating a cautious optimism among investors. In contrast, US markets are currently under pressure, with the Nasdaq 100 down -1.58% at 29229.49, reflecting a broader risk-off sentiment as tech stocks face headwinds. The S&P 500 is down -0.32% at 7513.45, while the Dow Jones remains relatively stable, down just -0.01% at 53050.36. This disparity highlights the ongoing volatility in the tech sector, which is grappling with hawkish signals from the Federal Reserve, as indicated by Fed’s Williams stating that “monetary policy is in a good place.” In the commodities space, crude oil prices are buoyed by supply deficits, with WTI up +1.88% at 69.8400 and Brent up +1.90% at 73.3600, while gold has rebounded modestly, up +0.73% at 4185.6001, despite the prevailing hawkish rhetoric from the Fed. Looking ahead, the market will be closely watching upcoming economic data releases, particularly any signals from the Fed regarding interest rate adjustments, which could further influence market sentiment and volatility across both equities and commodities.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6362.83 | -0.55% |

| DAX | 25631.47 | -0.72% |

| FTSE 100 | 10730.68 | +0.74% |

| CAC 40 | 8494.28 | +0.17% |

| FTSE MIB | 52895.84 | -0.12% |

| IBEX 35 | 19789.60 | +0.54% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7513.45 | -0.32% |

| Dow Jones | 53050.36 | -0.01% |

| Nasdaq 100 | 29229.49 | -1.58% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 68256.96 | -2.12% |

| Shanghai Composite | 3990.24 | -1.26% |

| Hang Seng | 23496.89 | -0.51% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.14 | -0.08% |

| GBP/USD | 1.34 | -0.11% |

| USD/JPY | 161.88 | -0.12% |

| Gold (XAU/USD) | 4185.60 | +0.73% |

| Crude Oil (WTI) | 69.84 | +1.88% |

| Brent Oil | 73.36 | +1.90% |

| Bitcoin | 62890.98 | -1.73% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by central bank signals and economic data. The Federal Reserve's stance, articulated by Williams, suggests that monetary policy is stable, which may temper expectations for aggressive rate hikes. This is juxtaposed with mixed economic data, notably the US ADP Employment Change 4-week average dropping to 20K, indicating potential softness in the labor market. In commodities, aluminium prices are buoyed by short supply amid Gulf outages, while oil prices are supported by deficits, indicating strong demand against constrained supply. Gold is experiencing a modest rebound despite hawkish Fed rhetoric, with ongoing buying from the People's Bank of China providing additional support. The Japanese Yen faces pressure from fiscal concerns and a dovish tone from the Bank of Japan, complicating its outlook. Meanwhile, the Canadian Dollar is consolidating as USD positioning stretches, and the Bank of Canada is expected to maintain its policy stance through 2026. The Euro remains steady as traders evaluate the paths of the Fed and ECB, with limited support from spreads.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 02:00 | Lloyds House Price Index (MoM) (Jun) | Medium |

| 02:00 | Lloyds House Price Index (YoY) (Jun) | Medium |

| 02:00 | German Industrial Production (MoM) (May) | Medium |

| 04:30 | Mortgage Rate (GBP) (Jun) | Medium |

| 05:30 | BoE Financial Stability Report | Medium |

| 05:30 | BoE MPC Meeting Minutes | Medium |

| 06:30 | BoE Gov Bailey Speaks | Medium |

| 07:00 | FOMC Member Bowman Speaks | Medium |

| 08:14 | ADP Employment Change Weekly | Medium |

| 08:15 | ADP Employment Change Weekly | Medium |

| 08:30 | Exports (May) | Medium |

| 08:30 | Imports (May) | Medium |

| 08:30 | Trade Balance (May) | Medium |

| 08:30 | Trade Balance (May) | Medium |

| 10:00 | Ivey PMI (Jun) | Medium |

| 11:00 | NY Fed 1-Year Consumer Inflation Expectations (Jun) | Medium |

| 11:30 | Atlanta Fed GDPNow (Q2) | Medium |

| 12:00 | EIA Short-Term Energy Outlook | Medium |

| 12:15 | BoE MPC Member Mann Speaks | Medium |

| 13:00 | 3-Year Note Auction | Medium |

| 16:30 | API Weekly Crude Oil Stock | Medium |

| 19:50 | Adjusted Current Account (May) | Medium |

| 19:50 | Current Account n.s.a. (May) | Medium |

| 21:30 | Building Approvals (MoM) (May) | Medium |

| 22:00 | RBNZ Interest Rate Decision | High |

| 22:00 | RBNZ Rate Statement | Medium |

| 23:00 | RBNZ Press Conference | Medium |

A series of economic reports and central bank communications are set to be released, including the Lloyds House Price Index and German Industrial Production, which may influence housing and manufacturing sectors. The Bank of England's Financial Stability Report and MPC Meeting Minutes, along with speeches from key officials, could impact market sentiment regarding monetary policy. Additionally, the RBNZ's interest rate decision and accompanying statements will be closely watched for implications on currency and investment flows, potentially leading to increased volatility in the markets.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.