European Markets Rally: EuroStoxx 50 Up 1.04% — Positive Momentum Ahead of US Open

· Market News · MarketsFN Team

🌍 European Markets Rally: EuroStoxx 50 Up 1.04% — Positive Momentum Ahead of US Open

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

**European Markets Rally on ECB Rate Hike Expectations Amidst Mixed US Data** European indices are showing a robust performance as the market digests the implications of a likely European Central Bank rate hike. The EuroStoxx 50 is up +1.04% at 6097.69, with the FTSE MIB leading gains at +1.44% (50491.95). The CAC 40 and DAX also posted solid increases of +0.71% (8204.80) and +0.36% (25092.41), respectively. This bullish sentiment is largely driven by a services-driven inflation rise in the euro area, which supports the ECB's tightening narrative, as highlighted by Societe Generale. In the US, markets are slightly positive, with the S&P 500 up +0.21% at 7616.28 and the Dow Jones gaining +0.30% (51231.94). However, the Nasdaq 100 is lagging slightly, up +0.31% (30609.00), reflecting a cautious approach as investors digest the latest JOLTS Job Openings data, which surged to a two-year high, indicating a tight labor market that could bolster the US Dollar. In the FX and commodities space, the EUR/USD is trading at 1.1644 (+0.06%), while gold prices are up +1.29% at 4533.1001, benefiting from geopolitical tensions and a supportive environment for safe-haven assets. Conversely, crude oil prices are under pressure, with WTI down -0.48% at 91.7200, despite an inventory drawdown that typically supports prices. Looking ahead, the market will be closely watching the upcoming US inflation data, which could significantly influence both the Federal Reserve's and ECB's monetary policy trajectories. A stronger-than-expected inflation print could validate the current rate hike expectations and further impact market dynamics.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6097.69 | +1.04% |

| DAX | 25092.41 | +0.36% |

| FTSE 100 | 10365.11 | +0.25% |

| CAC 40 | 8204.80 | +0.71% |

| FTSE MIB | 50491.95 | +1.44% |

| IBEX 35 | 18260.10 | +0.41% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7616.28 | +0.21% |

| Dow Jones | 51231.94 | +0.30% |

| Nasdaq 100 | 30609.00 | +0.31% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 66934.33 | +0.91% |

| Shanghai Composite | 4075.10 | +0.43% |

| Hang Seng | 26038.32 | +2.52% |

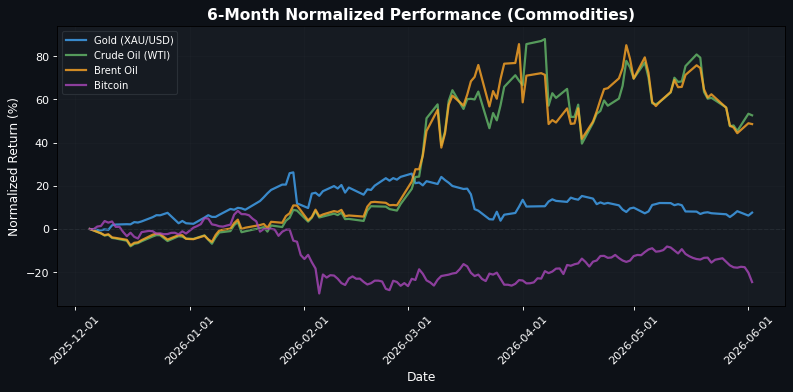

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.16 | +0.06% |

| GBP/USD | 1.35 | +0.10% |

| USD/JPY | 159.89 | +0.18% |

| Gold (XAU/USD) | 4533.10 | +1.29% |

| Crude Oil (WTI) | 91.72 | -0.48% |

| Brent Oil | 94.74 | -0.25% |

| Bitcoin | 67423.82 | -5.46% |

🌍 Geopolitics and Market Drivers

Current market dynamics are significantly influenced by geopolitical tensions and central bank signals. The Polish central bank's decision to maintain rates amidst geopolitical risks highlights concerns in Eastern Europe, while the Canadian Dollar remains stable near recent highs against the US Dollar, indicating resilience in the face of global uncertainties. In the Eurozone, the European Central Bank (ECB) is poised for an inevitable rate hike, driven by rising services-driven inflation, as noted by Societe Generale. This sentiment is echoed by Nordea, which anticipates an extension of the ECB's hiking cycle due to persistent inflationary pressures. In the U.S., JOLTS Job Openings surged to a two-year high, suggesting a robust labor market that could bolster the US Dollar, while manufacturing resilience raises inflation risks, according to MUFG. Oil prices are supported by inventory drawdowns, but geopolitical risks, particularly related to Iran, continue to create volatility, as highlighted by DBS and ING. The Japanese Yen remains under pressure, nearing intervention territory, reflecting broader market anxieties.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 01:50 | FOMC Member Kashkari Speaks | Medium |

| 02:30 | GDP (YoY) (Q1) | Medium |

| 03:00 | Spanish Unemployment Change (May) | Medium |

| 04:00 | IPC-Fipe Inflation Index (MoM) (May) | Medium |

| 05:00 | Core CPI (YoY) (May) | Medium |

| 05:00 | CPI (YoY) (May) | High |

| 05:00 | CPI (MoM) (May) | Medium |

| 09:30 | Interest Rate Decision (Jun) | Medium |

| 10:00 | BoE Gov Bailey Speaks | Medium |

| 10:00 | JOLTS Job Openings (Apr) | High |

| 16:30 | API Weekly Crude Oil Stock | Medium |

| 20:30 | S&P Global Services PMI (May) | Medium |

| 21:30 | GDP (QoQ) (Q1) | Medium |

| 21:30 | GDP (YoY) (Q1) | Medium |

| 21:45 | RatingDog Services PMI (May) | Medium |

A series of significant economic events are scheduled, including speeches from FOMC Member Kashkari and BoE Governor Bailey, which may influence market sentiment regarding interest rates and monetary policy. Key inflation metrics such as the CPI and Core CPI, along with GDP data, will provide insights into economic health and could lead to volatility in financial markets, particularly in interest rate-sensitive sectors. Additionally, the JOLTS Job Openings report and crude oil stock data may impact labor market perceptions and energy prices, respectively.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.