EuroStoxx 50 Rises 2.02%: European Markets Strong Ahead of US Open

· Market News · MarketsFN Team

🌍 EuroStoxx 50 Rises 2.02%: European Markets Strong Ahead of US Open

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

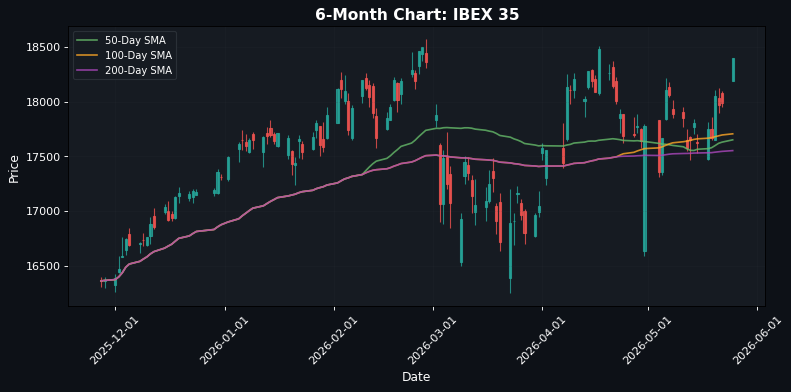

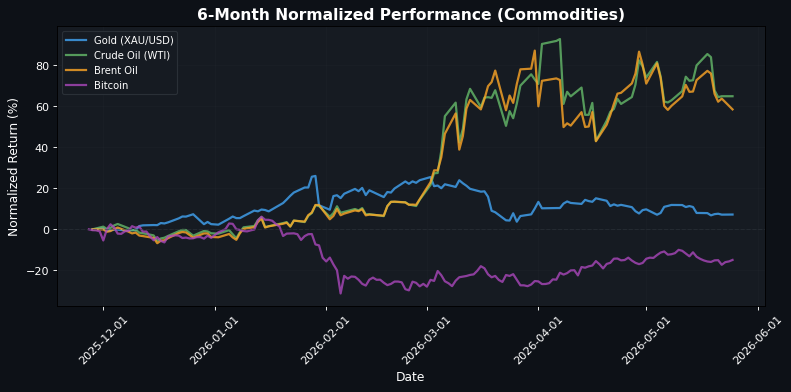

**European Indices Surge Amid Optimism, US Markets Follow Suit with Modest Gains** European markets are closing on a high note, driven by a wave of optimism that has seen the EuroStoxx 50 rise by +2.02% to 6140.82, with the DAX and CAC 40 also posting impressive gains of +1.94% and +1.92%, respectively. The IBEX 35 led the pack with a +2.29% increase, reflecting strong investor sentiment across the region. This bullish momentum appears to be fueled by hopes surrounding potential diplomatic resolutions, particularly regarding the US-Iran negotiations, which have contributed to a weaker US Dollar and buoyed gold prices. In the US, markets are experiencing a more tempered response, with the S&P 500 up +0.37% to 7473.47 and the Dow Jones gaining +0.58% to 50579.70. The Nasdaq 100 is also in the green, climbing +0.42% to 29481.64. The divergence between the robust European performance and the more cautious US gains suggests that investors may be underpricing the potential for geopolitical developments to impact market dynamics significantly. In the FX and commodities space, the EUR/USD is trading at 1.1648, up +0.24%, while Brent Oil has taken a hit, down -3.22% to 100.2100, reflecting concerns over supply amid the geopolitical backdrop. Gold remains resilient, inching up +0.05% to 4523.2002, as investors seek safe-haven assets. Looking ahead, the key catalyst to watch will be the outcome of the ongoing US-Iran negotiations. Any significant breakthrough could further shift market sentiment, potentially driving European indices even higher while impacting US market dynamics.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6140.82 | +2.02% |

| DAX | 25371.23 | +1.94% |

| FTSE 100 | 10466.30 | +0.22% |

| CAC 40 | 8271.26 | +1.92% |

| FTSE MIB | 50242.00 | +1.48% |

| IBEX 35 | 18397.70 | +2.29% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7473.47 | +0.37% |

| Dow Jones | 50579.70 | +0.58% |

| Nasdaq 100 | 29481.64 | +0.42% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 65158.19 | +2.87% |

| Shanghai Composite | 4152.57 | +0.96% |

| Hang Seng | 25606.03 | +0.86% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.16 | +0.24% |

| GBP/USD | 1.35 | +0.50% |

| USD/JPY | 158.90 | +0.08% |

| Gold (XAU/USD) | 4523.20 | +0.05% |

| Crude Oil (WTI) | 96.60 | +0.00% |

| Brent Oil | 100.21 | -3.22% |

| Bitcoin | 77647.69 | +0.87% |

🌍 Geopolitics and Market Drivers

Current market dynamics are significantly influenced by geopolitical developments surrounding the US-Iran negotiations. Hopes for a potential peace deal have led to a rebound in gold prices and a decline in the US Dollar and WTI Oil, which has fallen to two-week lows sub-$90.00. However, progress on the deal appears to be slowing, as noted by the Wall Street Journal, creating uncertainty. Central bank signals are also pivotal. The Bank of Canada is adopting a patient approach towards reaching a neutral policy stance, while the Bank of Korea is facing hawkish risks due to currency weakness. This backdrop suggests a cautious stance from central banks amid fluctuating economic conditions. In Asia, the South Korean Won is under pressure, and the Japanese Yen struggles despite a weaker US Dollar, largely due to elevated energy costs. Meanwhile, the Canadian Dollar's losses against the US Dollar are deemed limited by Scotiabank, indicating resilience. Overall, these geopolitical and macroeconomic factors are shaping a complex landscape for currencies and commodities, with implications for risk sentiment across markets.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 01:00 | Core CPI (YoY) (Apr) | Medium |

| 01:00 | CPI (YoY) (Apr) | Medium |

| 08:30 | Wholesale Sales (MoM) (Apr) | Medium |

The release of the Core CPI and overall CPI for April at 01:00 is expected to provide insights into inflation trends, which could influence monetary policy decisions and market sentiment. A higher-than-expected CPI may lead to increased volatility in equity and bond markets as investors adjust their expectations for interest rate hikes. Additionally, the Wholesale Sales data at 08:30 will further inform market participants about consumer demand and economic health, potentially impacting stock prices and sector performance.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.