EuroStoxx 50 Up 1.10%: European Markets Rally Ahead of US Trading Session

· Market News · MarketsFN Team

🌍 EuroStoxx 50 Up 1.10%: European Markets Rally Ahead of US Trading Session

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

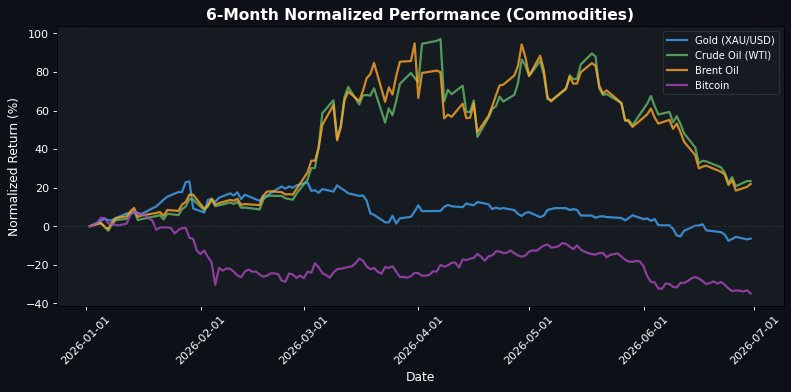

**European Indices Surge Amidst Global Optimism, US Markets Follow Suit** European markets are closing on a high note, with the EuroStoxx 50 up +1.10% at 6300.18, driven by strong performances across major indices. The DAX leads the charge, gaining +1.21% to 24925.62, while the FTSE MIB and FTSE 100 also show solid gains of +0.79% and +0.54%, respectively. This bullish sentiment is echoed in the US, where the S&P 500 is up +0.35% at 7466.20, and the Nasdaq 100 is performing even better with a +1.05% increase to 30087.23. The market's optimism appears to be fueled by a recalibration of risk perceptions, particularly in the context of sticky inflation and Fed skepticism highlighted in recent news. The US JOLTS Job Openings data, indicating resilient demand for workers, may further bolster this sentiment. However, the FX landscape shows some caution, with the EUR/USD down -0.26% at 1.1400 and the GBP/USD slipping -0.28% to 1.3220, reflecting concerns over potential intervention risks in the Japanese Yen and broader currency volatility. In commodities, gold is stabilizing after hitting a seven-month low, currently at 4039.0000 (+0.42%), while Brent Oil has gained +1.24% to 74.0600, despite economists lowering 2026 oil price forecasts due to improved shipping conditions in the Strait of Hormuz. Looking ahead, the upcoming US JOLTS Job Openings report will be pivotal. A stronger-than-expected reading could reinforce the current bullish trend in equities, while any signs of weakness might trigger a reassessment of market positions, particularly in the context of Fed rate-hike expectations.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6300.18 | +1.10% |

| DAX | 24925.62 | +1.21% |

| FTSE 100 | 10540.41 | +0.54% |

| CAC 40 | 8376.48 | +0.11% |

| FTSE MIB | 51565.60 | +0.79% |

| IBEX 35 | 19423.40 | +0.19% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7466.20 | +0.35% |

| Dow Jones | 52229.54 | +0.09% |

| Nasdaq 100 | 30087.23 | +1.05% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 70062.32 | +0.86% |

| Shanghai Composite | 4094.40 | +0.50% |

| Hang Seng | 22881.02 | -0.63% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.14 | -0.26% |

| GBP/USD | 1.32 | -0.28% |

| USD/JPY | 162.49 | +0.38% |

| Gold (XAU/USD) | 4039.00 | +0.42% |

| Crude Oil (WTI) | 70.75 | +0.00% |

| Brent Oil | 74.06 | +1.24% |

| Bitcoin | 58626.53 | -2.51% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by central bank signals and economic data releases. The Japanese Yen faces intervention risks, as highlighted by ING, amid warnings of potential government action to stabilize the currency. Concurrently, the US Dollar shows modest upside potential as recalibrated risks emerge, according to OCBC. Gold prices have steadied after hitting a seven-month low, pressured by Fed rate-hike expectations, with Commerzbank noting a significant quarterly loss due to Fed repricing. The recent US JOLTS Job Openings data is anticipated to reveal resilient labor demand, which could further influence Fed policy. In Europe, the Bank of England is expected to maintain its current stance through 2026, while Germany's annual CPI inflation softened to 2.3% in June, below the 2.5% forecast, indicating easing price pressures. Additionally, a Reuters poll shows lowered oil price forecasts for 2026, reflecting improved shipping conditions in the Strait of Hormuz. These factors collectively signal a cautious yet responsive market environment, influenced by central bank policies and geopolitical stability.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 02:00 | Business Investment (QoQ) (Q1) | Medium |

| 02:00 | Current Account (Q1) | Medium |

| 02:00 | GDP (QoQ) (Q1) | High |

| 02:00 | GDP (YoY) (Q1) | High |

| 02:00 | German Retail Sales (MoM) (May) | Medium |

| 02:45 | French Consumer Spending (MoM) (May) | Medium |

| 02:45 | French CPI (MoM) (Jun) | Medium |

| 02:45 | French HICP (MoM) (Jun) | Medium |

| 03:00 | KOF Leading Indicators (Jun) | Medium |

| 03:55 | German Unemployment Change (Jun) | Medium |

| 03:55 | German Unemployment Rate (Jun) | Medium |

| 04:40 | ECB's Elderson Speaks | Medium |

| 05:40 | ECB's Schnabel Speaks | Medium |

| 07:30 | Gross Debt-to-GDP ratio (MoM) (May) | Medium |

| 07:30 | ECB's Lane Speaks | Medium |

| 08:00 | German CPI (MoM) (Jun) | High |

| 08:00 | German CPI (YoY) (Jun) | Medium |

| 08:30 | GDP (MoM) (Apr) | Medium |

| 08:31 | GDP (MoM) (May) | Medium |

| 09:00 | S&P/CS HPI Composite - 20 n.s.a. (YoY) (Apr) | Medium |

| 09:00 | S&P/CS HPI Composite - 20 n.s.a. (MoM) (Apr) | Medium |

| 09:30 | ECB's Lane Speaks | Medium |

| 09:45 | Chicago PMI (Jun) | High |

| 10:00 | CB Consumer Confidence (Jun) | High |

| 10:00 | JOLTS Job Openings (May) | High |

| 12:03 | GDP Monthly (YoY) (May) | Medium |

| 16:30 | API Weekly Crude Oil Stock | Medium |

| 19:50 | Tankan All Big Industry CAPEX (Q2) | Medium |

| 19:50 | Tankan Big Manufacturing Outlook Index (Q2) | Medium |

| 19:50 | Tankan Large Manufacturers Index (Q2) | Medium |

| 19:50 | Tankan Large Non-Manufacturers Index (Q2) | Medium |

| 21:30 | Building Approvals (MoM) (May) | Medium |

| 21:45 | RatingDog Manufacturing PMI (MoM) (Jun) | Medium |

A series of significant economic indicators are set to be released, including GDP data for Q1 and various consumer spending and inflation metrics from Germany and France, which may influence market sentiment regarding economic growth and inflation trends. The ECB officials' speeches could provide insights into future monetary policy, potentially affecting investor expectations. Overall, these events are likely to create volatility in the markets as traders react to the implications for economic health and central bank actions.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.