S&P 500 and Dow Jones Up 0.50%: US Markets Steady Ahead of Economic Data Release.

· Market News · MarketsFN Team

🌍 S&P 500 and Dow Jones Up 0.50%: US Markets Steady Ahead of Economic Data Release.

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

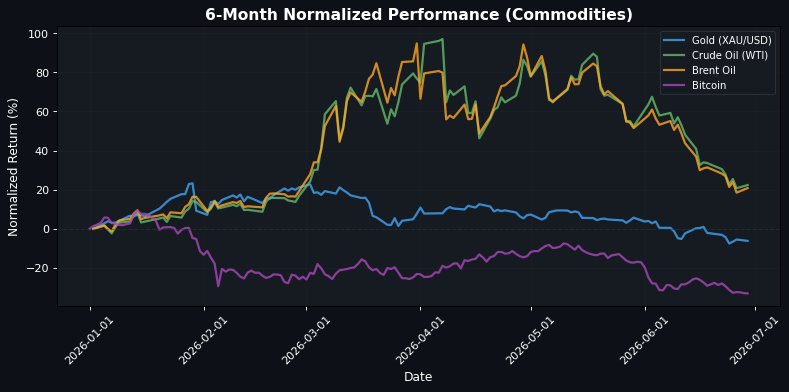

**European Markets Show Resilience Amidst Mixed Signals; US Indices Continue to Climb** European indices are exhibiting a modest upward trend as the session approaches its close, with the EuroStoxx 50 gaining +0.28% to 6239.17. The DAX and CAC 40 also posted gains of +0.19% and +0.08%, respectively, reflecting a cautious optimism despite underlying macro risks, particularly from heatwaves impacting economic growth in the Eurozone, as noted by ING. Conversely, the IBEX 35 slipped slightly by -0.06%, indicating a divergence in regional performance. In the US, indices are currently on an upward trajectory, with the S&P 500 and Dow Jones both up +0.50%, while the Nasdaq 100 leads with a +0.55% increase. This positive momentum is likely supported by a repricing of Fed rate hikes following softer inflation data, as highlighted by Deutsche Bank. The market appears to be underpricing the potential for sustained growth, especially in light of the cyclical drivers favoring the US Dollar, which is reflected in the EUR/USD trading at 1.1414, up +0.22%. Commodity markets are also responding to geopolitical dynamics, with WTI crude oil rising +1.31% to $70.14, buoyed by Gulf de-escalation news, while Brent oil surged +1.97% to $73.41. However, gold is under pressure, down -0.73% at $4048.80, indicating a shift in investor sentiment towards risk assets. Looking ahead, the market will be closely watching Kevin Warsh's remarks at Sintra, as any unexpected insights could significantly influence sentiment and trading strategies, particularly regarding the US Dollar and interest rate expectations.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6239.17 | +0.28% |

| DAX | 24718.37 | +0.19% |

| FTSE 100 | 10511.97 | +0.04% |

| CAC 40 | 8391.56 | +0.08% |

| FTSE MIB | 51279.25 | +0.03% |

| IBEX 35 | 19414.40 | -0.06% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7390.83 | +0.50% |

| Dow Jones | 52136.20 | +0.50% |

| Nasdaq 100 | 29279.23 | +0.55% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 69468.11 | +0.15% |

| Shanghai Composite | 4073.90 | +1.16% |

| Hang Seng | 23026.68 | +1.57% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.14 | +0.22% |

| GBP/USD | 1.32 | +0.24% |

| USD/JPY | 161.86 | +0.11% |

| Gold (XAU/USD) | 4048.80 | -0.73% |

| Crude Oil (WTI) | 70.14 | +1.31% |

| Brent Oil | 73.41 | +1.97% |

| Bitcoin | 59402.02 | -0.22% |

🌍 Geopolitics and Market Drivers

Current market dynamics are significantly influenced by geopolitical tensions and central bank signals. In the Eurozone, heatwaves are raising macroeconomic risks for growth, while the European Central Bank remains cautious about oil-driven inflation relief, indicating a complex outlook for monetary policy. The Euro is expected to show tactical strength against the US Dollar, supported by Sintra seasonality, despite cyclical Dollar strength posing risks. In the US, the Dollar Index reflects a repricing of Fed hikes due to softer inflation data, suggesting a potential shift in monetary policy expectations. The British Pound is gaining traction as Labour's Burnham commits to continuity in current policies, which may stabilize UK markets. Geopolitically, the situation in the Strait of Hormuz is creating uncertainty, with WTI Oil's decline stalling near $70.00, while Gulf de-escalation supports crude prices. Additionally, the Indian Rupee remains stable as investors await US-Iran talks in Oman, highlighting the ongoing geopolitical complexities that could impact currency markets.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 01:00 | BoE MPC Member Pill Speaks | Medium |

| 03:00 | Spanish CPI (YoY) (Jun) | Medium |

| 03:00 | Spanish HICP (YoY) (Jun) | Medium |

| 07:30 | RBA Assist Gov Kent Speaks | Medium |

| 13:30 | ECB President Lagarde Speaks | Medium |

| 19:50 | Industrial Production (MoM) (May) | Medium |

| 21:30 | RBA Meeting Minutes | Medium |

| 21:30 | Chinese Composite PMI (Jun) | Medium |

| 21:30 | Manufacturing PMI (Jun) | High |

| 21:30 | Non-Manufacturing PMI (Jun) | Medium |

Today's economic events include key speeches from central bank officials, such as BoE MPC Member Pill and ECB President Lagarde, which may influence market sentiment regarding monetary policy. Additionally, the release of Spanish CPI and HICP data, along with China's Composite and Manufacturing PMIs, will provide insights into inflation and economic activity, potentially impacting currency and equity markets. Overall, these events are likely to create volatility as investors react to signals about future economic conditions and central bank actions.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.