S&P 500 Rises 0.74%: US Markets Gain Momentum Amid Positive Sentiment — Bullish Outlook.

· Market News · MarketsFN Team

🌍 S&P 500 Rises 0.74%: US Markets Gain Momentum Amid Positive Sentiment — Bullish Outlook.

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

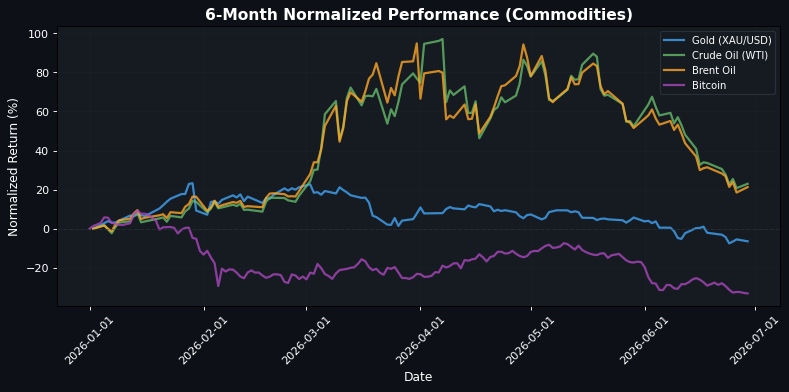

**US Markets Rally While European Indices Struggle Amid Global Economic Concerns** As US markets continue to gain momentum, with the S&P 500 up +0.74% at 7408.76 and the Nasdaq 100 leading the charge with a +1.12% increase to 29443.19, European indices are facing headwinds. The EuroStoxx 50 is barely in the green at +0.05%, while major indices like the DAX (-0.19%) and FTSE 100 (-0.14%) are struggling to maintain positive territory. This divergence highlights a growing concern over economic stability in Europe, particularly as heatwaves threaten growth, as noted by ING. The FX landscape reflects these tensions, with the Euro trading at 1.1425 against the US Dollar, up +0.31%, suggesting a tactical strength that may not be fully supported by underlying economic fundamentals. Meanwhile, the Japanese Yen is under pressure, testing 2024 lows against the Dollar, as Japan's export controls and strong sales create a risk premium, according to BNY. Commodities are also reacting, with crude oil prices rising—WTI up +1.82% to $70.49 and Brent oil up +2.35% to $73.68—indicating a potential shift in energy demand dynamics. Investors should be cautious as the market appears to be underpricing the implications of a slowing Chinese economy, which is weighing on the Chinese Yuan and could have ripple effects on global trade and growth. The upcoming remarks from Kevin Warsh at Sintra may serve as a critical catalyst; any insights into monetary policy shifts could either bolster US market confidence or exacerbate European economic fears.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6224.89 | +0.05% |

| DAX | 24624.21 | -0.19% |

| FTSE 100 | 10493.71 | -0.14% |

| CAC 40 | 8377.07 | -0.09% |

| FTSE MIB | 51143.09 | -0.24% |

| IBEX 35 | 19390.60 | -0.18% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7408.76 | +0.74% |

| Dow Jones | 52205.53 | +0.64% |

| Nasdaq 100 | 29443.19 | +1.12% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 69360.88 | -4.15% |

| Shanghai Composite | 4073.90 | +1.16% |

| Hang Seng | 23026.68 | +1.57% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.14 | +0.31% |

| GBP/USD | 1.32 | +0.30% |

| USD/JPY | 161.93 | +0.15% |

| Gold (XAU/USD) | 4035.80 | -1.05% |

| Crude Oil (WTI) | 70.49 | +1.82% |

| Brent Oil | 73.68 | +2.35% |

| Bitcoin | 59320.28 | -0.36% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by geopolitical and macroeconomic factors. The Chinese Yuan is under pressure due to a slowdown in China, impacting its value against the US Dollar, as noted by Commerzbank. In Japan, export controls and robust sales are creating a risk premium for the Japanese Yen, although it is testing 2024 lows against the Dollar, highlighting a fragile economic outlook (Societe Generale). The Canadian Dollar is stabilizing as spreads narrow, indicating a potential recovery (Scotiabank). Meanwhile, the US Dollar is experiencing strength driven by cyclical factors and a repricing of Fed hikes in response to softer inflation data (Deutsche Bank). The Eurozone faces macro risks from heatwaves affecting growth, while oil prices are supported by geopolitical stability in the Gulf, despite a stall in WTI crude near $70.00 due to uncertainties in the Strait of Hormuz (BNY). Political developments in the UK are also noteworthy, as the British Pound gains traction following Labour's commitment to current policies. Overall, these factors suggest a complex interplay of economic signals and geopolitical risks shaping market sentiment.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 01:00 | BoE MPC Member Pill Speaks | Medium |

| 03:00 | Spanish CPI (YoY) (Jun) | Medium |

| 03:00 | Spanish HICP (YoY) (Jun) | Medium |

| 07:30 | RBA Assist Gov Kent Speaks | Medium |

| 13:30 | ECB President Lagarde Speaks | Medium |

| 19:50 | Industrial Production (MoM) (May) | Medium |

| 21:30 | RBA Meeting Minutes | Medium |

| 21:30 | Chinese Composite PMI (Jun) | Medium |

| 21:30 | Manufacturing PMI (Jun) | High |

| 21:30 | Non-Manufacturing PMI (Jun) | Medium |

A series of significant economic events are scheduled, including speeches from key central bank officials such as BoE's Pill, RBA's Kent, and ECB's Lagarde, which may influence market sentiment and expectations regarding monetary policy. Additionally, the release of Spanish CPI and HICP data, along with China's Composite and Manufacturing PMIs, will provide insights into inflation and economic activity, potentially affecting currency and equity markets. Overall, these events could lead to increased volatility as traders react to the implications for interest rates and economic growth.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.