S&P 500 Drops 1.09% Amid Market Selloff: US Indices Struggle as Tech Leads Decline.

· Market News · MarketsFN Team

🌍 S&P 500 Drops 1.09% Amid Market Selloff: US Indices Struggle as Tech Leads Decline.

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

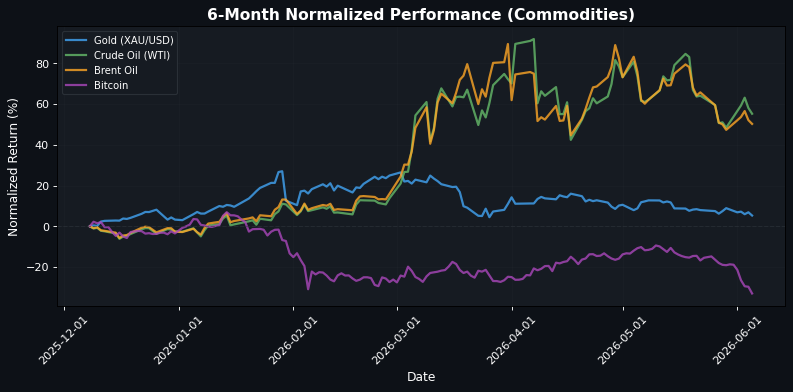

**Market Faces Pressure Amid Mixed Economic Signals and Strong Dollar** As European markets approach the close, the dominant theme is a notable risk-off sentiment, driven by a stronger US dollar and disappointing economic indicators. The EuroStoxx 50 is down 0.51% at 6072.13, reflecting broader concerns about growth, particularly after Eurozone GDP data suggested weaker economic performance. The DAX and FTSE MIB also fell, down 0.45% to 24831.55 and 0.39% to 49977.32, respectively. In contrast, the FTSE 100 and IBEX 35 managed slight gains, up 0.32% to 10393.91 and 0.48% to 18364.00, indicating a divergence in market sentiment across regions. In the US, the S&P 500 is down 1.09% at 7501.33, with the Nasdaq 100 leading the decline at -2.17% to 29746.98. The recent US Nonfarm Payrolls report, which showed an increase of 172K in May versus an expected 85K, has bolstered the dollar, pushing the EUR/USD down 0.36% to 1.1575 and the GBP/USD down 0.20% to 1.3400. This strength in the dollar is further reflected in the commodity markets, where gold has dropped 1.49% to 4409.2998 and crude oil prices have fallen, with WTI down 1.77% to 91.3900. The market appears to be underpricing the potential for further tightening from the European Central Bank, as indicated by Nomura's commentary on a recalibration phase starting with a June hike. A key forward-looking catalyst will be the upcoming inflation data, which could either reinforce or challenge the current narrative of a strong dollar and its implications for global markets.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6072.13 | -0.51% |

| DAX | 24831.55 | -0.45% |

| FTSE 100 | 10393.91 | +0.32% |

| CAC 40 | 8247.44 | +0.04% |

| FTSE MIB | 49977.32 | -0.39% |

| IBEX 35 | 18364.00 | +0.48% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7501.33 | -1.09% |

| Dow Jones | 51391.98 | -0.33% |

| Nasdaq 100 | 29746.98 | -2.17% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 66588.12 | -1.31% |

| Shanghai Composite | 4027.74 | -0.74% |

| Hang Seng | 24961.95 | -1.15% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.16 | -0.36% |

| GBP/USD | 1.34 | -0.20% |

| USD/JPY | 160.16 | +0.15% |

| Gold (XAU/USD) | 4409.30 | -1.49% |

| Crude Oil (WTI) | 91.39 | -1.77% |

| Brent Oil | 93.88 | -1.21% |

| Bitcoin | 60816.00 | -4.68% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by recent economic data releases and central bank signals. The US Nonfarm Payrolls report showed an increase of 172K in May, significantly surpassing the expected 85K, which has strengthened the US Dollar and raised concerns about potential structural headwinds for the currency, as noted by Nordea. The upbeat jobs report has also pushed USD/JPY back near intervention territory at 160.00. In the Eurozone, disappointing GDP data has led to a decline in the Euro against the Pound, indicating weaker growth prospects. The European Central Bank's signal of a June hike suggests a recalibration phase, which could impact future monetary policy. In commodity markets, improved US natural gas supply outlooks and declining oil inventories are tightening supply conditions, while aluminium supply strains raise concerns about demand destruction, as highlighted by Commerzbank. Additionally, the Australian Dollar's retreat reflects the broader strength of the US Dollar post-NFP report, impacting currency valuations globally. Overall, these factors create a complex landscape for investors navigating geopolitical and macroeconomic risks.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 00:30 | Interest Rate Decision | Medium |

| 02:00 | Halifax House Price Index (MoM) (May) | Medium |

| 02:00 | Halifax House Price Index (YoY) (May) | Medium |

| 03:00 | CPI (MoM) (May) | Medium |

| 03:00 | CPI (YoY) (May) | Medium |

| 03:30 | ECB Supervisory Board Member Tuominen Speaks | Medium |

| 04:30 | Mortgage Rate (GBP) (May) | Medium |

| 05:00 | GDP (QoQ) (Q1) | Medium |

| 05:00 | GDP (YoY) (Q1) | Medium |

| 06:30 | GDP Quarterly (YoY) (Q4) | Medium |

| 08:30 | Average Hourly Earnings (MoM) (May) | High |

| 08:30 | Average Hourly Earnings (YoY) (YoY) (May) | Medium |

| 08:30 | Nonfarm Payrolls (May) | High |

| 08:30 | Participation Rate (May) | Medium |

| 08:30 | Private Nonfarm Payrolls (May) | Medium |

| 08:30 | U6 Unemployment Rate (May) | Medium |

| 08:30 | Unemployment Rate (May) | High |

| 08:30 | Employment Change (May) | Medium |

| 08:30 | Unemployment Rate (May) | Medium |

| 10:00 | Ivey PMI (May) | Medium |

| 13:00 | U.S. Baker Hughes Oil Rig Count | Medium |

| 13:00 | U.S. Baker Hughes Total Rig Count | Medium |

| 14:00 | BoE Gov Bailey Speaks | Medium |

| 15:00 | Consumer Credit (Apr) | Medium |

| 15:30 | CFTC GBP speculative net positions | Medium |

| 15:30 | CFTC Crude Oil speculative net positions | Medium |

| 15:30 | CFTC Gold speculative net positions | Medium |

| 15:30 | CFTC Nasdaq 100 speculative net positions | Medium |

| 15:30 | CFTC S&P 500 speculative net positions | Medium |

| 15:30 | CFTC AUD speculative net positions | Medium |

| 15:30 | CFTC BRL speculative net positions | Medium |

| 15:30 | CFTC JPY speculative net positions | Medium |

| 15:30 | CFTC EUR speculative net positions | Medium |

A series of significant economic events are set to unfold, including interest rate decisions, various housing and inflation metrics, and employment data, all of which are likely to influence market volatility. Key indicators such as the CPI, GDP figures, and nonfarm payrolls will provide insights into economic health and may impact investor sentiment and central bank policies. Additionally, speeches from central bank officials could further shape market expectations, particularly regarding interest rates and monetary policy direction.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.