DAX Up 0.12% as Dow Jones Rises 0.38%: Mixed Sentiment in European and US Markets.

· Market News · MarketsFN Team

🌍 DAX Up 0.12% as Dow Jones Rises 0.38%: Mixed Sentiment in European and US Markets.

European markets approaching close (still trading) • US markets actively trading • Analysis based on last 8 hours

📊 Market Overview

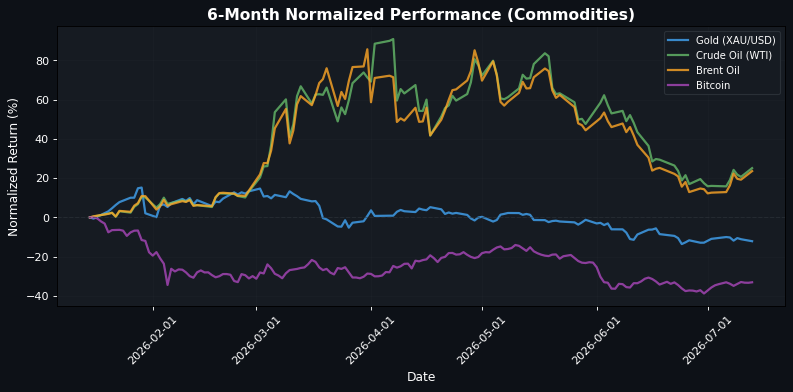

**Oil Prices Surge Amid Geopolitical Tensions, Impacting Broader Market Sentiment** As European markets approach the close, the dominant theme is the significant rise in oil prices, which has been fueled by renewed geopolitical tensions, particularly between the US and Iran. Crude oil (WTI) has jumped +3.70% to $74.0500, while Brent oil has increased +3.67% to $78.8000. This surge is likely contributing to a mixed performance across indices, with the DAX up +0.12% at 25097.53 and the CAC 40 gaining +0.27% to 8361.77, while the EuroStoxx 50 remains flat at 6269.96, down -0.00%. In the US, the S&P 500 is slightly down -0.15% at 7563.74, while the Dow Jones has managed a gain of +0.38% to 52837.83. The Nasdaq 100, however, is underperforming with a decline of -1.29% to 29440.53, reflecting a risk-off sentiment that may be linked to the broader concerns over inflation and geopolitical instability. In the FX markets, the US Dollar is supported by these geopolitical and inflation risks, with EUR/USD trading at 1.1418, down -0.09%. Gold has also seen a decline of -1.13% to $4057.6001, as investors pivot towards oil and equities amid these tensions. Looking ahead, the market will be closely watching for any developments regarding US-Iran relations, particularly any escalations that could further impact oil prices and, by extension, global market sentiment. A significant shift in this geopolitical landscape could either bolster or undermine the current market dynamics.

🇪🇺 European Markets (Approaching Close)

| Name | Price | Daily (%) |

|---|---|---|

| EuroStoxx 50 | 6269.96 | -0.00% |

| DAX | 25097.53 | +0.12% |

| FTSE 100 | 10502.16 | +0.05% |

| CAC 40 | 8361.77 | +0.27% |

| FTSE MIB | 52802.08 | +0.36% |

| IBEX 35 | 19382.90 | -0.01% |

🇺🇸 US Markets (Currently Active)

| Name | Price | Daily (%) |

|---|---|---|

| S&P 500 | 7563.74 | -0.15% |

| Dow Jones | 52837.83 | +0.38% |

| Nasdaq 100 | 29440.53 | -1.29% |

🌏 Asian Markets

| Name | Price | Daily (%) |

|---|---|---|

| Nikkei 225 | 67242.73 | -1.92% |

| Shanghai Composite | 3913.79 | -2.06% |

| Hang Seng | 24213.72 | +0.16% |

💱 FX & Commodities

| Name | Price | Daily (%) |

|---|---|---|

| EUR/USD | 1.14 | -0.09% |

| GBP/USD | 1.34 | -0.12% |

| USD/JPY | 162.20 | +0.35% |

| Gold (XAU/USD) | 4057.60 | -1.13% |

| Crude Oil (WTI) | 74.05 | +3.70% |

| Brent Oil | 78.80 | +3.67% |

| Bitcoin | 63995.74 | +0.37% |

🌍 Geopolitics and Market Drivers

Current market dynamics are heavily influenced by geopolitical tensions and central bank signals. The Federal Reserve's stance on inflation risks and its decision to hold policy steady is pivotal, as it shapes expectations for future rate hikes. Concurrently, rising hostilities between the US and Iran, particularly regarding the Strait of Hormuz, are elevating oil prices and creating uncertainty in energy markets. This geopolitical backdrop supports the US Dollar, as noted by MUFG, while the Euro has climbed above 1.1400 against the Dollar, indicating a shift in market sentiment. In Switzerland, the Swiss National Bank's cautious policy stance and potential intervention are keeping the Swiss Franc stable against the Euro, with forecasts suggesting it will remain around 0.9200. The Japanese Yen is experiencing elevated volatility due to the GPIF narrative, while the New Zealand Dollar faces scrutiny over potential RBNZ tightening. Overall, these factors create a complex macroeconomic landscape, with central bank policies and geopolitical risks driving currency fluctuations and market sentiment.

📅 Today's Economic Calendar

All times are in US Eastern Time (ET)

| Time (ET) | Event | Importance |

|---|---|---|

| 03:00 | Turkish Retail Sales (MoM) (May) | Medium |

| 03:00 | Turkish Retail Sales (YoY) (May) | Medium |

| 05:25 | FOMC Member Bowman Speaks | Medium |

| 06:00 | OPEC Meeting | Medium |

| 06:30 | CPI (YoY) (Jun) | Medium |

| 12:30 | Fed Waller Speaks | Medium |

| 12:45 | ECB's Schnabel Speaks | Medium |

| 14:00 | BoE MPC Member Pill Speaks | Medium |

| 14:00 | Federal Budget Balance (Jun) | Medium |

| 17:00 | ECB President Lagarde Speaks | Medium |

| 18:00 | NZIER Business Confidence (Q2) | Medium |

| 19:01 | BRC Retail Sales Monitor (YoY) (Jun) | Medium |

| 21:30 | NAB Business Confidence (Jun) | Medium |

| 23:00 | Exports (YoY) (Jun) | Medium |

| 23:00 | Imports (YoY) (Jun) | Medium |

| 23:00 | Trade Balance (USD) (Jun) | Medium |

The release of Turkish retail sales data, both monthly and yearly, could indicate consumer spending trends and impact the Turkish lira, while speeches from various central bank officials, including FOMC and ECB members, may influence market sentiment regarding interest rate policies. Additionally, the OPEC meeting and subsequent economic indicators like CPI, trade balance, and business confidence reports will likely affect commodity prices and overall market stability, particularly in relation to inflation expectations and trade dynamics. Overall, these events are expected to create volatility in both currency and equity markets as investors react to potential shifts in monetary policy and economic health.

Disclaimer

The content on MarketsFN.com is provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or trading guidance. All investments involve risks, and past performance does not guarantee future results. You are solely responsible for your investment decisions and should conduct independent research and consult a qualified financial advisor before acting. MarketsFN.com and its authors are not liable for any losses or damages arising from your use of this information.